The Big Bad Wolf (market correction) came along, so he huffed and puffed, and blew down the houses made of straw and sticks, but he couldn`t blow down the house made of stone (picture source)

Disseminated on behalf of Commerce Resources Corp. and Zimtu Capital Corp.

When Commerce Resources Corp. attended the Argus Metal Pages REE Conference a month ago in Denver, Colorado, they were the only REE junior present that was active on their project. Yes, there were other REE juniors in attendance, but these were companies working on new technologies, as alternatives to the industry standard of solvent extraction (SX). And no, Commerce Resources is not looking for success from any new technologies as standard processing works very efficiently for Ashram.

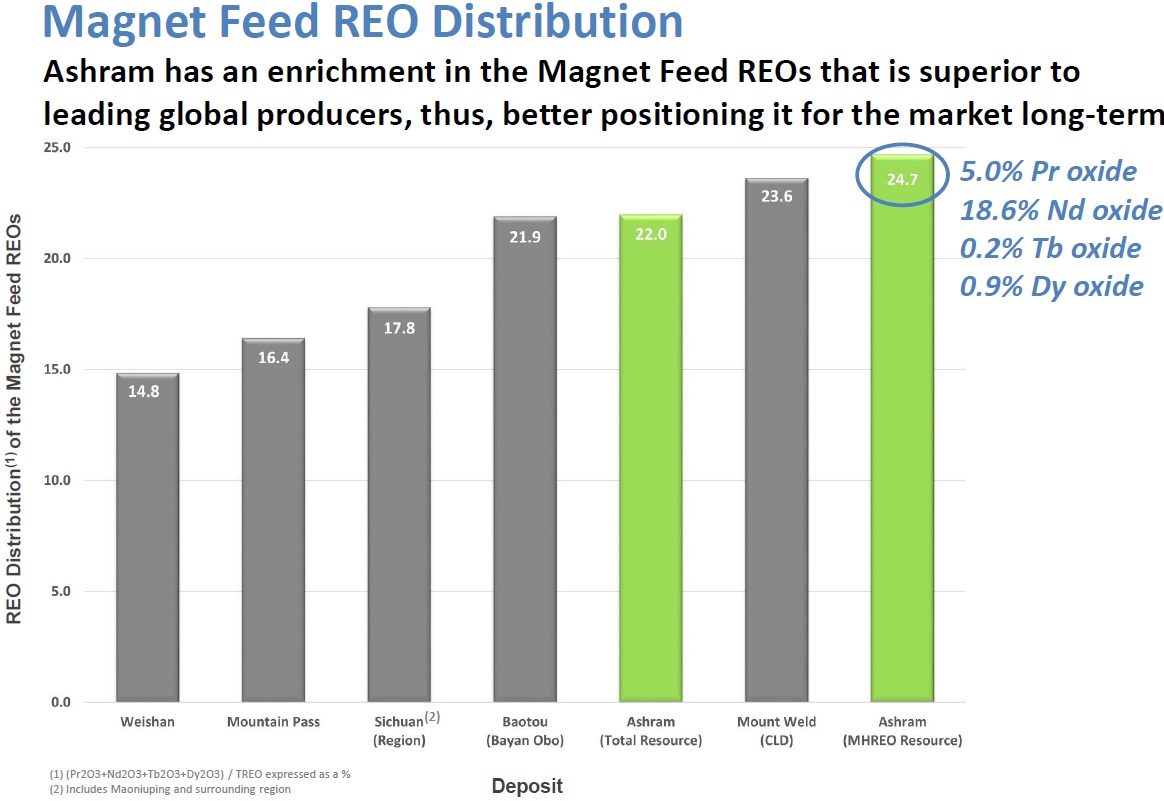

No doubt, the REE market has changed dramatically in the last 5 years, and the main takeaway from this conference is something that would probably surprise most market pundits. It’s that everyone can see the exponential drop in prices over the last 5 years, but very few realize that actual REE demand and usage have increased over the same time period. These seemingly contradictory trends, with lower prices not being a reflection of lowered demand, is something highly unusual, and the simple answer for this behaviour is that prices went too high in the aftermath of the panic in the streets following the Senkaku boat incident and the Chinese cutting off supplies to Japan. Additionally, the fallout from 2011 means that there has been at least one general design change in the permanent magnets and their REE recipe, coming from the work of Siemens. This change of recipe has reduced the percentage amount of dysprosium being used – a negative to any REE junior whose economics are mostly tied into the value of dysprosium – and then the concomitant percentage increase in either neodymium or praseodymium. This means that the REE market has actually morphed into being even more in line with the distribution of the Ashram Deposit than it was previously – a deposit which has a leading global enrichment in those magnet feed REOs.

Comparing the Ashram REE Deposit of Commerce Resources Corp. with the majority of active global REE producers demonstrates that Ashram has fundamentals that could give it arguably the best economics of all known REE development projects. The reasoning behind this seemingly bold statement is quite simple:

Ashram shares the similarities of geology and mineralogy with the majority of REE producers, including the Chinese majors. For that reason, Commerce does not need to look for a new technology (or a “Hail Mary Pass”, as the other juniors are doing). In this respect, it should not surprise that more than 80% of current global REO production is dominated by the rock type carbonatite. Thus, if you want to build a successful REE company you need to make sure you have the right (carbonatite) foundation, otherwise your chances are dim to say the least.

While over 150 rare earth minerals exist, only 4 have been commercialized: Monazite, bastnaesite, xenotime and loparite, out of which the first 3 account for more than 80% of global REO production (current and historic), with the remainder being dominated by the ion-absorption type clay deposits in China. Being commercialized is the key point here, in that only those minerals out of a total of more than 150 have been processed at a profit. Further, only monazite, bastnaesite and xenotime mineralogies are amenable to producing high-grade mineral concentrates of >40% REO. As Ashram is a carbonatite deposit enriched in those 3 REE minerals, it has been able to demonstrate successfully, and repeatedly, its ability to produce high-grade (>45% REO) mineral concentrates at high recoveries (>75%). The same is true for most other global REE producers, current and historic.

The second takeaway is that the REE market demand has actually increased over the last years while at the same time prices have dropped – and this is a highly unusual, if not Black Swan type of event.

The third point to consider is that the change in magnet recipe has actually turned the largest sector of demand for REEs further towards the natural distribution of the Ashram Deposit. The result is that dysprosium is needed less and that neodymium or praseodymium is needed more. Ashram is a global leader in those magnet feed REOs. Dysprosium is enriched at Ashram, providing a nice spice to the deposit’s leading enrichment in neodymium and praseodymium. Ashram’s well-balanced distribution is anchored firmly in the magnet feed REOs which have the most stable long-term market fundamentals.

Bottom-line: Ashram is the only REE deposit in development that has all of the ingredients needed to go into production (when compared with historic and current producers on a global scale):

1) the right foundation (carbonatite host rock)

2) the right minerals (commercialisable/processable minerals)

3) the right elements (marketable products in high demand)

Company Details

Commerce Resources Corp.

#1450 - 789 West Pender Street

Vancouver, BC, Canada V6C 1H2

Phone: +1 604 484 2700

Email: cgrove@commerceresources.com

www.commerceresources.com

Shares Issued & Outstanding: 250,008,529

Canadian Symbol (TSX.V): CCE

Current Price: $0.075 CAD (August 2, 2016)

Market Capitalization: $19 million CAD

German Symbol / WKN (Frankfurt): D7H / A0J2Q3

Current Price: €0.047 EUR (August 2, 2016)

Market Capitalization: €12 million EUR

Analyst Coverage

Research #18 “REE Boom 2.0 in the making?“

Research #17 “Quebec Government starts working with Commerce“

Research #16 “Glencore to trade with Commerce Resources“

Research #15 “First Come First Serve“

Research #14 “Q&A Session About My Most Recent Article Shedding Light onto the REE Playing Field“

Research #13 “Shedding Light onto the Rare Earth Playing Field“

Research #12 “Key Milestone Achieved from Ashram’s Pilot Plant Operations“

Research #11 “Rumble in the REE Jungle: Molycorp vs. Commerce Resources – The Mountain Pass Bubble and the Ashram Advantage“

Research #10 “Interview with Darren L. Smith and Chris Grove while the Graveyard of REE Projects Gets Crowded“

Research #9 “The REE Basket Price Deception & the Clarity of OPEX“

Research #8 “A Fundamental Economic Factor in the Rare Earth Space: ACID“

Research #7 “The Rare Earth Mine-to-Market Strategy & the Underlying Motives“

Research #6 “What Does the REE Market Urgently Need? (Besides Economic Sense)“

Research #5 “Putting in Last Pieces Brings Fortunate Surprises“

Research #4 “Ashram – The Next Battle in the REE Space between China & ROW?“

Research #3 “Rare Earth Deposits: A Simple Means of Comparative Evaluation“

Research #2 “Knocking Out Misleading Statements in the Rare Earth Space“

Research #1 “The Knock-Out Criteria for Rare Earth Element Deposits: Cutting the Wheat from the Chaff“

Disclaimer: Please read the full disclaimer within the full research report as a PDF (here) as fundamental risks and conflicts of interest exist.