Full size / The woolly mammoth, one of the last in a line of mammoth species, was driven to extinction by climate change and human impacts. The image depicts a late Pleistocene landscape in Spain with 4 woolly mammoths, a woolly rhinoceros, equids, and European cave lions with a reindeer carcass. Painting by Mauricio Antón. (Source)

Disseminated on behalf of Emerita Resources Corp. and Zimtu Capital Corp.

Last week, Emerita Resources Corp. released the first batch of assays from its maiden drilling program at the Infanta Deposit of the Iberian West Project in Andalusia, Spain. This week, more drill results are expected to be released. With 2 drill rigs already in action, and a third one planned to be added, a steady newsflow is in the making. Having closed a $20 million bought-deal financing in mid-July, the company is in a strong position to advance its projects in Spain and become one of the most active exploration and development companies in the Iberian Pyrite Belt – home to some of the world‘s largest VMS deposits.

Made-in-USA (but not Mined-in-USA): While Donald Trump pushed to speed up domestic mining projects, US President Joe Biden prefers to rely on its ally countries Canada, Australia and Brazil, among others, to mine most of the critical minerals needed to make the “green wave“ a success. Instead of focussing to permit more mines in the US, the Biden Administration plans to be more focused on creating jobs that process critical minerals domestically (e.g. electric vehicle battery parts).

Europe Goes Mining: The EU aims to take a different approach, with initiatives to rebuild its economy for the time after COVID-19 that include mining as well as processing of minerals domestically in the EU. The “Next Generation EU” fund, a €750 billion EUR rescue package for member states hit by the COVID-19 pandemic, was requested to make a strategic investment of €3.1 billion EUR for mine development and related activities in the Andalusian part of the Iberian Pyrite Belt in Spain.

For more than a quarter century, mining giants Rio Tinto and its 45%-minority joint-venture partner BHP have been holding hands in an effort to get permitted the Resolution Copper Project near Superior, Arizona, to become one of the world‘s largest underground mines supplying about 25% of US copper demand with >60 years of mine-life. The project targets a deep-seated porphyry copper deposit (1600 million t @ 1.47% copper) at depths exceeding 1,300 m. Having spent $2 billion since 2004, without yet having produced any copper, both Rio Tinto and BHP are eager to spend another $6 billion to bring Resolution Copper into production. However, the permitting struggle continues, at least for the next little while, putting the Resolution Copper Project on hold once again: “It appears that the Biden administration is not going to pay attention to domestic mineral production for communities like Superior,“ said Mila Besich (Mayor of Superior) in May 2021.

Not only mayors but also miners in the US are “very disappointed“ to learn that the Biden Administration is considering importing raw materials from abroad rather than pursuing mining opportunities at home. On the other side of the pond, the opposite appears on the horizon, where political climate is brightening up for mining: “The pandemic has highlighted the risks associated with the interruption of international supply chains and, to avoid this situation occurring in the future, Europe is looking at being self-sufficient, as opposed to the current position which sees most raw materials for economic activities being imported from outside the zone.“

To do so, the EU needs a fair amount of metals in the ground along with a scalable mining industry. Luckily, Europe is home to the world‘s largest known concentration of massive sulphides hosting the much sought-after “green metals“ within the Iberian Pyrite Belt in southwestern Spain and Portugal. Spain‘s “problem child“, Andalusia, is on track to become Europe‘s flagship mining hub, showcasing economic recovery and growth with environmentally sound practices hand in hand with the creation of new jobs, investment opportunities and prospects for a better future.

Full size / “The Iberian Pyrite Belt (IPB), with more than 80 known deposits containing >1700 Mt of sulphide ore (mined and reserves), is one of the largest (if not the largest) of the world‘s massive sulphide provinces... Compared with other world-class provinces, especially on an equal-area basis, the IPB stands out clearly as a “monster“ in terms of relative metal weight; its sulphide and metal tonnages are far greater, and the Neves-Corvo deposit alone is comparable to the whole of the Canadian and Australian provinces... With more than 80 known deposits, the IPB sulphide resources (ore mined + reserves) are in excess of 1700 Mt, totalling 14.6 Mt Cu [32 billion lbs], 13.0 Mt Pb, 34.9 Mt Zn, 46.1 Kt Ag [1.5 Boz] and 880 t Au [28 Moz]). Moreover, numerous deposits in the IPB were traditionally mined only for pyrite and their polymetallic potential was commonly not recognized; improved knowledge of these deposits will probably increase the known sulphide tonnage significantly and improve the metal potential of the belt, as has been indicated recently by the discovery or confirmation of extensions to the old mines of Aguas Tenidas, Concepcion, La Zarza and Tharsis. Furthermore, the potential of the IPB is still open for sophisticated exploration at depth, as is shown by the discovery of blind deposits such as Gaviao, Lagoa Salgada, Neves-Corvo, Cabezo Migollas, Los Frailes, Valverde and Las Cruces...“ [Cont‘d below]

Full size / “ [...] Mining has been active in the belt since the Chalcolithic era with the result that today almost all the outcropping and near-surface deposits are exhausted and mineral prospecting must now orientate itself towards finding deeper orebodies. The fact that pyrite is no longer used as a raw material for manufacturing sulphuric acid, combined with the rather poor known base-metal content of the deposits, has resulted in many mines closing over the last two decades... It was the 1977 discovery of Neves-Corvo with its Cu and Sn-rich orebodies that led to renewed exploration interest in the area. This deposit was a major discovery, not only because Neves-Corvo is a deep blind deposit, but because the richness of the deposit showed that the Iberian Pyrite Belt still contains major economic metal potential; subsequent renewed exploration has already resulted in further orebodies being discovered. The other interesting aspect of the mining revival is that the Iberian Pyrite Belt has also become a major field area for worldwide scientific research, research that has harvested a wealth of new data, that has given rise to new metallogenic concepts, and that has led to revised geological interpretations not only of this province, but of the entire Western Hercynides.“ (Source: “The volcanic-hosted massive sulphide deposits of the Iberian Pyrite Belt”, 1998)

Back to the Roots: The Mother of all Elephant Countries

50 million years ago, the African plate pushed into the European plate forcing some mountains upwards and others underneath the earth‘s crust. A large section dropped off into the earth‘s liquid mantle causing the crust to dip and rocks to twist. This brought deeply buried sulfide-rich material to the surface, which was deposited 350 million years ago (Devonian Period) by active and hydrothermal volcanism in submarine environments. The result: An unparalled depository of mineral wealth in form of volcanic- and sediment-hosted massive sulfide (VSHMS) deposits, a hybrid between VMS (volcanogenic massive sulfide) and SEDEX (sedimentary exhalative) deposits.

Full size / A Atalaya open pit (Rio Tinto), looking west, massive sulphides show up as dark areas; B Lago open pit (Rio Tinto), looking west, massive sulphides were in the pit, forming the core of a syncline, and stockwork is still visible on both sides of the pit; drifts are of Roman age; C quartz-sulphide veins of the San Dionisio stockwork, Atalaya open pit (Rio Tinto), the green colour of host rhyolite results from chloritization; D La Zarza open pit, looking east, massive sulphides show up as dark areas with a complex geometry; E San Platon open pit, sulphide lenses are blue-grey and the host acidic volcanite is strongly sericitized; the presence of several lenses could be of tectonic origin; F pyritic stockwork of the San Miguel open pit, sulphide veins are grey-green and the red colour of chloritized host acidic volcanic is an oxidation patina from meteoric water. (Source: “The volcanic-hosted massive sulphide deposits of the Iberian Pyrite Belt”, 1998)

“The Iberian Pyrite Belt (IPB) has been one of the major mining districts in Europe since prehistoric times. It is an area of significant geological and metallogenic interest because it represents the largest concentration of metallic sulfide deposits on Earth. With more than 2000 Mt of massive sulfide ore, the IPB comprises an exceptional number of supergiant deposits, including the biggest in this class: Riotinto (>500 Mt) and Neves Corvo (≥300 Mt).“ (Source: “Massive Sulfide Ores in the Iberian Pyrite Belt“, 2019)

“The Iberian Pyrite Belt (IPB) is one of the largest volcanic/sediment-hosted massive sulphide (VSHMS) provinces including more than 88 known deposits, representing the largest sulfur and iron crustal anomaly on Earth. Some of those deposits are considered giant in size, e.g., Neves-Corvo, Aljustrel, Lousal and São Domingos (in Portugal) and Rio Tinto, Tharsis, Sotiel and Aznalcóllar (in Spain), comprising ca. 2000 Mt of massive sulfides. Identical metallogenetic provinces, such as Val d´Or (Canada) and the Mount Read Belt (Tasmania), are also hosted in a Volcanic Sedimentary Complex (VSC) sequence as IPB polymetallic mineralizations. Due to its base metal occurrences, the IPB has been subject of numerous mineral exploration programs in the last decades, which have gathered a huge volume of geological, geochemical and geophysical data.“ (Source: “Geochemistry of Iberian Pyrite Belt“, 2020

Mammoth Land

The Iberian Pyrite Belt is a 250 km long and 30-50 km wide mountain range running northwest to southeast from Alcacer do Sal (Portugal) to Seville (Spain). The mines located on the shores of the Rio Tinto river in the Huelva province of Andalusia, Spain‘s southernmost autonomous community, are reputed to be the oldest mines in the world. And that‘s where it all began, at least for Rio Tinto Company.

The Rio Tinto river rises at the historic Riotinto Mine site, the birthplace and namesake of today‘s 2nd highest valued mining company by market capitalization. (Image)

In 1872/1873, a multinational consortium of investors purchased the mine complex on the Rio Tinto river from the Spanish Government and created a company by the name of Rio Tinto. After working the Riotinto Mines for about 80 years and a long series of mergers and acquisitions, Rio Tinto Ltd. grew to the world‘s 2nd most valuable metals and mining company today with a market capitalization of $174 billion AUD (BHP Group Ltd: $244 billion AUD). “The company‘s name comes from the Rio Tinto in southwestern Spain, which has flowed red since mining began there about 5,000 years ago, due to acid mine drainage.“

The source of the 100 km long Rio Tinto river in the heart of the Iberian Pyrite Belt is also the source for more than 5,000 years of mining: The famous Riotinto Mines, where copper, silver, gold and other minerals have been extracted as far as 20 km from the river shores. As an indication of the scope of acient mining: 16 million t of Roman slag have been identified near the Rio Tinto river: “As a possible result of the mining, the Río Tinto [river] is notable for being very acidic (pH 2) and its deep reddish hue is due to iron dissolved in the water [“Tinto“ in Spanish means 1) “tainted“ and 2) “red“]. The Riotinto mines have been worked since Phoenician and Roman times and were leased to a Swede named Wolters in 1725 and to a British syndicate in 1873: “Production declined after the peak of production in 1930. The mines were returned to Spanish control in 1954 and were considered to be among the world’s most valuable copper mines for many decades. Low copper prices caused the mines to close in 2002, but many of the mines were reopened in 2007. Much of the copper from the mines is transferred to chemical plants in Huelva province. The refined copper and other minerals are exported through the port in Huelva city.“

Full size / “The late Roman and early medieval periods continued to take advantage of the richness of the River Tinto and its surroundings. The Arabs completed this first stage in the 13th century, when they lost the place. This was followed by a long period of inactivity despite attempts at reopening led by Philip II. The English revival of Riotinto: During the 18th century it was extracted again. Foreign influence was decisive from the beginning. For example, in the first quarter of that century it was a Swede, Liberto Wolters, who led the extraction project. Different employers would eventually make the mine profitable. Industrialization would further encourage this after the difficult years of the War of Independence. Thus, there was a before and after in 1873. That was when the creation of the Rio Tinto Company Limited was completed... In the more than 80 years of the Rio Tinto Company Limited, millions of tons of material were extracted... After several readjustments of the company in charge, everything went well until the 1980s. Then a crisis affected the mining business, destroying practically all possible competitiveness. With the price of metal at rock bottom, the activity declined until 1995 when the exploitation passed into the hands of the workers. This happened as a result of a curious pact in which the company sold the shares for one peseta. Despite the efforts, in 2001 the machinery was shut down. During this forced impasse Minas de Riotinto was forced to change... Industrial activity returned in 2015 thanks to a company from Cyprus. Atalaya Mining took advantage of the upturn in copper and other metals...“ (Source: “The Riotinto Mines, 2000 years of mining in a Martian environment“)

Andalusia: A Reborn Metallic Mining Giant

Excerpts from OECD‘s Rural Study “Mining Regions and Cities Case of Andalusia, Spain“ (2021):

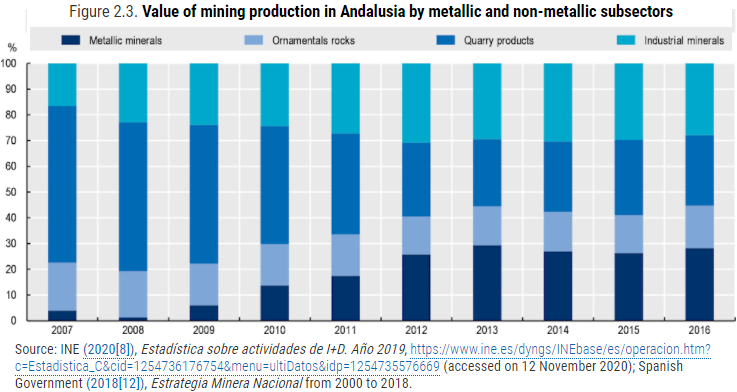

Andalusia has been a mining force throughout history because of its great geodiversity. The extraction activity in Andalusia dates back to no less than 5 000 years ago... The early 2000s put an end to the prosperity of the mining sector, with a slowdown that lasted 10 years in which no work was done in the metallic mining sector. Spanish metallic mines closed down due to the downward fluctuations of metal prices. In the period 2007-12, the extractive mining sector experienced a decrease of 60.43% in its volume of production. After the financial crisis, the trend changed in Andalusia. The region experienced a growth in mining production, whose share over the national production rose from 18.4% in 2010 to 25.8% in 2013... Andalusian mining continues to grow as the global market has entered a new period with increasing international demand for minerals.

Mining, a great opportunity for regional development in Andalusia: The present offers a scenario of strategic opportunity for mining in Andalusia. Andalusia has the largest European reserve of non-ferrous minerals with nearly 470 active companies and mining operations [mostly quarries] that produce 41 million tonnes per year. Mining industry directly employs more than 7 400 people, especially relevant in a region of Spain facing high levels of unemployment... Andalusia has multiplied by 14 the value of its mining production since 2000. In Andalusia, the reopening of mines – especially of the region of Huelva – has led the current mining value production to expand from EUR 90.8 million in 2000 to generate EUR 1 346 million in 2018.

Full size / “In 2018, Andalusia accounted for the vast majority of the total national production value of metal ores, as the spearhead of the country... Andalusia, the southernmost region of Spain, has the largest population and second-largest land area in the country. It is the lead mining region in Spain in terms of production (38.6% of mining production) and employment (28.4%). Andalusia is also a growing player in the European mining sector, distinguishing itself as the second European producer of copper and leader in the production of marble and gypsum. The region’s location in the Iberian Pyrite Belt (IPB), encompassing Seville and Huelva through to Southern Portugal, represents a global asset when it comes to metallic minerals. Within the region, Huelva is the main mining (TL3) region, producing 70% of the region’s metallic mining. Andalusia hosts companies and activities at almost every stage of the mining value chain, from extractive to processing activities as well as technology and service providers. It benefits from two distinct mining subsectors, each with an extended supply chain. The metallic mining sector (copper, zinc and lead) accounts for most of the regional mining production and is largely made up of branches of large foreign-based companies. In contrast, the non-metallic sector (ornamental rocks, aggregates and industrial minerals) is highly dispersed across the territory and is composed of small local family businesses.“ (Source: “Mining Regions and Cities Case of Andalusia, Spain“, OECD, 2021)

Full size / Source: “Mining Regions and Cities Case of Andalusia, Spain“, OECD, 2021

The Andalusian provinces of Huelva and Sevilla take up almost 60% of the IPB, while the remaining 40% is located in the Portuguese region of Alentejo. This mining resource has more than 82 active mines [and undeveloped deposits and prospects] prospectsfor resources that are estimated at more than 1 600 Million tonnes of massive sulphides and 2 500 Mt of mineralisation in stock, constituting one of the most important metallogenic provinces in the world and considered one of the deposits with the highest concentration of sulphides in the planet. Overall, Huelva accounts for most of the region’s metal production (70%), followed by Seville (30%) which contains the remaining part.

The rising value of some metals, together with the presence of ores in Andalusia, form a scenario of strategic opportunity for the increasing recovery of mining. In Andalusia, copper in particular is increasingly sought after due to the high demand in building clean energy technologies and from industrial processes in Asian countries. In this context, exploration in the entire IPB has expanded and led to the reopening of old mines such as Aguas Teñidas, Riotinto or Sotiel and new ones such as Cobre Las Cruces, while La Zarza, Lomero, San Telmo or Tharsis, among others, are in viability studies...

Full size / “[...] the European Union (EU) is increasingly urging countries to make the most of its mineral resources and transformation process to enhance industrial resilience and support the transition to a low-carbon economy. Along that path, Spain and particularly Andalusia are well placed, as several key materials for the transition can be found and exploited in its territories, such as aluminium, cobalt, tin, graphite, lithium, manganese, nickel, gold, silver, rare earths and tungsten. Therefore, Andalusia has the possibility to be a frontrunner and position itself as a key player in the European mining scenario.“ (Source: “Mining Regions and Cities Case of Andalusia, Spain“, OECD, 2021)

Andalusia is the largest mining producer in Spain, the second-largest copper producer in the EU and a leader in marble and gypsum production. The region benefits from two distinct mining subsectors, each with a rich network of suppliers that are relevant for local development: the metallic mining sector (e.g. copper and zinc), which accounts for most of the regional mining production, and the non-metallic sector (ornamental rocks, aggregates and industrial minerals), which is highly dispersed across the territory. The regional mining value chain has the potential to leverage the increasing global and EU demand for sustainable raw materials and thus become a frontrunner in leading technologies and circular processes for environmentally sustainable mining. This study identifies how Andalusia can build on its strengths and address current and future challenges to improve regional productivity and well-being while accelerating the transition to a low-carbon economy and assisting EU climate goals...

The region has the potential to further mobilise the assets of its mining ecosystem to attract investment and open new sources of growth while meeting EU climate goals. These assets include attractive geology, a strategic geographic location among EU and non-EU markets, good infrastructure and benefits from the proximity of mines to urban centres (e.g access to services). Furthermore, the region enjoys a mining identity with a young workforce that offers community support for mining ventures...

Full size / “Andalusia has a strong workforce as its population is young, standing out from comparable OECD regions. In particular, the province of Huelva is significantly above the TL3 benchmark for mining regions and this characteristic is one of Huelva‘s strengths for future prosperity. However, an ageing and shrinking workforce has accompanied recent years of stagnant population growth. As a result, the scenario is prosperous for the region of Andalusia, whereas it is important to capitalise on the demographic bonus by mobilising the labour force – particularly youth – to contribute to the labour market.“ (Source: “Mining Regions and Cities Case of Andalusia, Spain“, OECD, 2021)

The European Union’s new priorities, driven by the Green Deal, the new Industrial Strategy and the Raw Materials Strategy, will stimulate the future demand for sustainable raw materials in Europe and support programmes to develop environmentally friendly mining value chains to attain climate neutrality by 2050. This represents an opportunity for Andalusia to leverage its mining sector and become a frontrunner in the development of clean energy technologies and circular processes to support a reliable supply of sustainable raw materials...

European countries and regions with the right mining potential and know-how have a unique opportunity to benefit from these European strategies and their support programmes to unlock new growth opportunities... Certain European mining regions, such Andalusia, and their business ecosystems are well-positioned to meet this technological demand through a low-carbon production process across the mining value chain. Andalusia is in fact one of those regions that are instrumental for the EU strategy of raw materials. As mentioned in previous chapters, Andalusia is the largest mining producer in Spain and holds the greatest deposits of metallic minerals in the country, which includes copper, a basic material for power transmission. The region stands out by its foreign-based mining and transformative business ecosystem that has invested in installed capacity and technology to extract and transform minerals in line with high environmental standards...

Full size / Source: “Mining Regions and Cities Case of Andalusia, Spain“, OECD, 2021

The increasing global demand and strategic EU support for sustained access to raw materials represents an opportunity for Andalusia. The mining ecosystem in Andalusia presents a number of strengths that can be further mobilised to become a frontrunner in resource circularity and environmentally sustainable mining. They include:

• Attractive geology. Andalusia’s subsoil has diverse geology and, after many years of mining, remains highly prospective. It covers 60% of the IPB and holds the largest European reserve of non-ferrous minerals. Andalusia’s mineral deposits contain some quantities of minerals identified as critical to supporting the generation of clean energy technologies (e.g. zinc, lead, silver, nickel, cobalt, copper, molybdenum, manganese) and a rich mining endowment (more than 400 mines) that provides a fertile ground for technologies to recover traditional and critical minerals.

• A strategic geographic location as the closest EU region to Africa and with cultural proximity to Latin America. Africa and Latin America are important sources of minerals for Europe as well as relevant mining markets that also seek greater environmentally friendly mining practices. Responsible sourcing initiatives coupled with EU support for sustainable mining practices provide Andalusia with a competitive advantage to engage with African and Latin American mineral producers and become a gateway to and from the EU in sustainable mining processes and technologies.

• Good infrastructure and proximity of mines to urban centres. Andalusia’s mining potential sits close to large urban centres, which provides the bonus of not having to operate in isolation, unlike many mining projects in other OECD regions. Logistics, health, safety and personnel matters are all greatly simplified by having urban centres closely at hand. The region also benefits from a reliable transport (roads, railroads and ports) and energy (sound mix of energy sources, with a share of renewables) infrastructure. Yet, work remains to be done to enhance the quality of the infrastructure (e.g. broadband) and the co-ordination among infrastructure plans and the mining strategy.

• A marked mining identity with a young workforce that offers community support for mining ventures. According to the 2018 INFACT survey (3 000 citizens), 60% of Spaniards showed an attitude between neutral and positive towards mineral exploration, which is relatively higher than in other European countries (Finland, Germany). Despite the impact on perception after the environmental disaster in the Aznalcóllar Mine at the end of the 1990s, Andalusian communities kept recognising the benefits of mining for the local economy and regional development.

Full size / Corta Atalaya, an open cut at the Riotinto Mines, massive sulphides in dark (Image) “The Rio Tinto mines [are] one of the most famous mining districts in the world for the size of the mineralization and for its intense history: it has been worked discontinuously for about 5000 years by the Tartessians, Phoenicians, Romans, Arabs, British and Spanish. The high geological interest of this mining district is because it is most probably the biggest sulphur anomaly on the Earth’s crust, with original tonnages around the 2500 million tons of mineralized rock in different degrees. A fifth of it was massive sulphides with an average content of 45% S, 40% Fe, 0.9% Cu, 2.1% Zn, 0.8% Pb, 0.5 g/t Au and 26 g/t Ag... The mineralization is found either as dissemination or small veins in the stockwork areas within volcanic rocks and slates, or as massive sulphide lenses lying atop or included in the stockwork zones, or in gossan areas representing the supergenic alteration of massive sulphides, sometimes up to 70 m thick.“ (Source: “The Iberian Pyrite Belt“, 2008)

Excerpts from “Huelva And Sevilla Iberian Pyrite Belt Mining Project Can Create 6,800 Jobs“ (April 4, 2021):

It is reported that officials from the Ministry of Economic Transformation have been in advanced talks during recent months with the Next Generation, about this macro-project, in the hope of being able to get the required funding and the go-ahead for it very soon, which can make it a key to kickstarting the economy of Andalucía after the pandemic. The proposed project will see the mining, transformation, and recovery of metals that are part of the group of fundamental raw materials listed by the European Commission to lead the economic and digital transition, as this enclave has huge resources of sulfide deposits, including copper, zinc, lead, silver, and gold, as well as mineralisations of cobalt, and others of gallium, indium, and germanium... The minerals which can be mined from the Iberian Pyrite Belt in Huelva and Sevilla are the basis for the manufacture of electrical and electronic equipment for mobiles, computer equipment, electricity storage batteries, and solar panels, as well as being used in equipment for electric vehicles, as reported by juntadeandalucia.es.

The Regional Government of Andalusia, Junta de Andalucia, stated in its press-release (“noticia“) “La Junta presenta a los Next Generation un proyecto minero de 3.100 millones para la Faja Pirítica“ (April 4, 2021; excerpts loosely translated from Spanish):

The Ministry of Economic Transformation, Industry, Knowledge and Universities has promoted a 3.1 billion Euro project for the metal mining and metallurgy sectors in Andalusia to apply for funds from the European Union‘s Next Generation program. This large-scale project, which is located in the Iberian Pyrite Belt, between the provinces of Seville and Huelva, brings together some 20 industrial and infrastructure investments led by the 6 main companies operating in this industrial segment. The sustainable use of metallic minerals and the use of clean energy sources are the main pillars of the initiative, the start-up of which is associated with the generation of an estimated 6,800 jobs.

Most of the actions identified in this macro-project are in advanced stages of administrative processing, which will allow these to be implemented in the short term. This is why the Ministry of Economic Transformation has been working in recent months with both industrial segments to attract the funds associated with Next Generation. This is a public push that could be decisive for the materialisation of these investments in 2 areas that are a driving force for the revitalisation and growth of Andalusian industry and its driving companies and which could be key to the economic recovery of Andalusia after the pandemic.

Moreover, this high level of progress is an additional advantage that strengthens the region‘s candidacy compared to other geographical locations, bearing in mind that these actions are driven by multinational companies... These actions presented to the European fund will launch new metal recovery processes that are not currently being exploited through various technological patents. In addition, the projects foresee the incorporation of renewable sources in energy generation, especially photovoltaic energy and the use of biomass, which will be applied both in the processes and in the facilities used. Similarly, the initiatives contemplate the promotion of industrial and mining alliances that will be able to strengthen European supply chains and will consolidate Andalusia and Spain as an international benchmark.

Also, among the proposed measures are the recovery of critical metals such as cobalt, indium and zinc contained in primary and secondary materials; obtaining precious metals from ores, and recovering palladium and platinum concentrates. It also includes extractive activity and on-site treatment for the production of refined metals or high value-added products such as copper, zinc, lead, gold and silver, as well as technological development initiatives in mineral concentration processes. Likewise, the environmental regeneration of degraded areas is included, through a low-carbon mining operation...

The mining sector in Andalusia has 464 active operations [most of which are non-metallic quarries], which have made the region a national benchmark in the production of materials such as copper, iron oxide, plaster or marble. According to the latest statistics published by the Ministry of Ecological Transition, in 2018 the Andalusian mining sector represented 39% of the value of national production, reaching 1,359 million Euro. In recent years, this sector has been experiencing spectacular growth, in which the metal subsector stands out in first position. Precisely, this catalyst project presented by Andalusia to the Next Generation fund will favor the support of this industry, which aspires to lead Andalusian industrial growth. According to the data provided by [...] AMINER..., Andalusian metal mining genrated income of 3,200 million Euro in 2019 and has registered exports worth 1,700 million Euro. This business segment, which generates 10,000 direct jobs and up to 30,000 indirect jobs, has processed 17 million tons of mineral ore annually. Obviously, in 2020, the pandemic had a negative impact on the data in that respect.

As announced by Emerita Resources Corp. in April 2021: “The Junta of the Andalucia Region passed a law designating underground mining as a strategically important industry in the region that will be permitted in all areas of the region. Mining development will have priority as an economic activity.“ David Gower, Emerita‘s CEO, stated: “These initiatives are important and send a strong message with respect to the importance of mining to the Andalucía region and the contribution the region can make in terms of providing domestic European supply of strategic minerals. Emerita has long recognized the advantages of mining investments in this area. The geological potential is well established by a mining history that dates back to at least the Roman times and continues to have production from modern, leading edge operations. The area has significant advantages due to exceptional infrastructure, highly educated and productive professionals, access to post secondary institutions and well established mining and permitting regulations. These competitive advantages will be further enhanced by these recent announcements. Emerita is investigating how this just announced program may apply to its projects.”

Apparently, authorities in Andalusia (and Brussels) have recognized that after thousands of years of mainly open-pit mining in the region, it‘s better to now focus on underground mining. And that‘s not only because VMS-type deposits tend to expand at depth, but also because open-pit mining poses much higher environmental risks: At underground mines, the tailings (waste material from mining and processing) usually go back underground as paste fill and is not stored above ground in large ponds at risk of failure due to liquefaction of the tailings dam. Also, the tonnage is much lower as only high-grade material is selectively mined and processed, leaving behind much less waste. As such, open-pit projects in Andalusia may face permitting challenges in the future, while underground mines are encouraged, and possibly subsidized, in an EU-driven effort to make Spain shine again for the benefit of the EU and its member states.

Iberian Pyrite Belt: Grade, Scale and Scalability, and Infrastructure

The renowned Iberian Pyrite Belt is one of the most productive VMS terranes in the world. Infrastructure and access is exceptional.

The Iberian Pyrite Belt, home to large-scale mining and exploration projects, including:

First Quantum Minerals Ltd. (TSX: FM; MC: $18 B) operates (Cobre) Las Cruces, a high-grade open-pit (2020-Inferred: 34.4 Mt @ 1.12% Cu, 2.64% Zn, 1.23% Pb, 28.83 g/t Ag); annual production: up to 72 kt Cu cathode @ on-site hydromet refining plant specifically designed for its polymetallic VMS ore rich in chalcocite, 2020: 1.46 Mt milled @ 4.35% Cu, recovery 85%, 54 kt Cu cathode.

Lundin Mining Corp. (TSX: LUN; MC: $8 B) mines underground Neves-Corvo from 5 major orebodies / 7 massive sulfide lenses; 2 plants at its processing facility (annual capacity: 2.6 Mt Cu ore + 1.1 Mt Zn or Cu ore (expansion to 2.5 Mt since 2017 for annual average of 150 kt Zn concentrate over 10 years); 2021 Guidance: 35 kt Cu + 70 kt Zn @ $2.2/lb Cu; 2017 reserves: 29 Mt @ 2.6% Cu, 0.7% Zn, 0.2% Pb, 34 g/t Ag (Copper Zone) + 34 Mt @ 7.5% Zn, 0.4% Cu, 1.8% Pb, 66 g/t Ag (Zinc Zone); in 02/2009, Lundin closed sale of Aljustrel to Portuguese holding company MTO SGPS SA for an undisclosed sum; Aljustrel was re-opened in 2008 after being on care and maintenance for more than a decade, expected to produce 80 kt of contained metal in concentrate per year, cost $225 M to build but mine uneconomic in 2008 due to low metal prices.

Atalaya Mining Plc (TSX: AYM; MC: $774 M) owns 100% of the Riotinto Mines District (virtual tour); 2016 commercial production started at the Cerro Colorado open pit (reserves: 650 kt Cu; M&I+I: 950 kt Cu); 2020 record production of 55,890 t Cu from processing 14.8 Mt with its plant @ 0.45% Cu; recovery: 85% ; reserves: 197 Mt; 2021 Guidance: 15.1 Mt throughput, producing 52 kt Cu @ $2.65 USD/lb AISC; adjacent deposits (100%): San Dionisio / Planes-San Antonio (historic non-43-101: 800 kt Cu, 1.2 Mt Zn, 750 koz Au, 56 Moz Ag); satellite deposit (100%): Masa Valverde (Inferred: 440 kt Cu, 1.3 Mt Zn, 1.3 Moz Au, 72 Moz Ag); Galicia, Spain: Proyecto Touro (up to 80%; permitting stage; reserves: 392 kt Cu, M+I+I: 680 kt Cu).

MATSA (private company, 50% Trafigura, 50% Mubdala since 2015 for estimated $500 M; both considering MATSA sale at estimated $2 B) operates 3 near-by underground mines in Huelva, all processed at its single plant (2019: 4.3 Mt ore/year; 1.8 Mt from Aguas Tenidas, 2 Mt from Magdalena, 0.5 Mt from Sotiel; 2020 total production: ~100 kt CuEq): Aguas Tenidas (discovered in 1980; first access ramp 1997, after 3 years of production the mine closed in 2001 (low metal prices), project acquired by Matsa‘s parent company in 2005, permitted in 2007, restart of commercial production in 2009; since 2006: >$1 B invested in construction and expansion projects at processing plant and outdoor facilities; Magdalena (7 km from Agua Tenidas facilities): discovered in 2013 by Matsa, research ramp in 2014, permit and commercial production since 2015; Sotiel (38 km from Aguas Tenidas): important mine since Roman times, mine closed in 2001, reopened in 2015 despite low grades.

Pan Global Resources Inc. (TSX.V: PGZ; MC: $98 M) develops the Escacena Project (exploration-stage; directly adjacent to Aznalcollar / Los Frailes), drilling 52.6 m @ 0.76% Cu, 0.05% Sn, 3.8 g/t Ag, 0.01 g/t Au (after 42.4 m core length) at La Romana Target (May 2021).

Ormonde Mining Plc (LSE: ORM; MC: 3 M GBP) operates La Zarza, historically a significant open-pit and underground mine closing in early 1990s; drilling by Ormonde and its (former) JV partner led to 9.9 Mt @ 10% Cu, 3% Zn, 1.6 g/t Au, 39 g/t Ag in underground resources (Indicated JORC, 2004), however mining concessions for project are held by Ormonde’s former JV partner.

Full size / “VMS are base metal-rich mineral deposits, which can also contain lesser amounts of precious metals. Their ores can be major sources of zinc, copper, and lead, with gold and silver as by-products. VMS deposits consist of massive or semi-massive accumulations of sulfide minerals which form as lens-like or tabular bodies parallel to stratigraphy or bedding. VMS deposits are found worldwide, and often form clusters, or camps. Several major VMS camps are known in Canada. These high-grade deposits are often in the range of 5 to 20 Mt but can be considerably larger. Some of the largest VMS deposits in Canada include the Flin Flon mine (62 Mt), the Kidd Creek mine (+100 Mt) and the Bathurst No. 12 mine (+100 Mt). During mid late 20th century the Iberian belt lose interest in favor of larger and lower cost discoveries being found in the Americas, Southeast Asia and Australia. Despite these circumstances the exploration continued up to the present day and the mining activities have accelerated again since the turn of the century resulting in several discoveries, some of which are current mines including Las Cruces (Seville), Aguas Teñidas (Huelva) and Río Tinto (Huelva) and various exploration projects are underway such as those in La Zarza, Lomero Poyatos or Masa Valverde. In Portugal, mining continued in Neves Corvo, and Aljustrel has been reopened.“ (Source)

Emerita Resources Corp. is the operator of 3 exploration and development projects in Spain, all of which have been obtained through the successful participation at public tenders initiated by the respective Spanish authorities, whereas Emerita hopes to get awarded a 4th public tender project, Aznalcollar / Los Frailes.

#1 Plaza Norte: In April 2017, the parliament of Cantabria (northern Spain) passed amendments to the law that regulates various land uses and created a solid legal framework intended to promote and attract mining activity in the region. Immediately following the enactment of these laws, the Government of Cantabria launched an exploration tender with the aim of attracting investment to the area of the Reocin Mine, which was active for almost 150 years, and the surrounding mining camp. The tender for the region encompassed a total of 460 claims (13,800 ha) which were previously controlled by Asturiana de Zinc, a subsidiary of Glencore in Spain until 2003, when the Reocin Mine ceased operation and the mining rights were returned to the Government of Cantabria. In October 2019, Emerita announced its successful tender bid. Cantábria del Zinc, a joint-venture company controlled by Emerita (50%) and Aldesa (50%, a major construction firm), was granted 120 claims (3,600 ha) which were strategically selected based on its detailed review of the historical data. The joint venture is focused on advancing a significant zinc project along with the government and community in Cantabria.

#2 Iberian Belt West (IBW; also referred to as Paymogo / La Romanera): This public tender was announced in November 2013. About 7 months later, the tender was resolved in favor of another bidder. Emerita considered its bid was not assessed fairly and appealed the resolution. After 5 years of fighting for its rights, the Supreme Court of Spain confirmed the ruling supporting Emerita‘s challenge to the IBW Project tender award and Emerita was officially notified in June 2020 through a resolution that it was the winning bidder, obtaining an exploration permit registered under the name of “La Romanera“; the property has been renamed by Emerita as “Iberian Belt West“ (IBW).

#3 Nuevo Tintillo: In May 2021, Emerita announced to have won the public tender process for the Nuevo Tintillo Property, located a few kilometers north of the property which includes the past producing Aznalcollar and Los Frailes open-pit mines.

(#4) Aznalcollar / Los Frailes: In 2014, Emerita participated in this public tender, which was awarded to another company in 2015. Emerita challenged the decision and is confident to get it awarded as three levels of courts in Spain have determined that crimes were committed during the tender process.

Iberian Belt West (IBW)

Emerita acquired 100% of the IBW Project through a public tender process (no cash payments for acquisition, no royalties). The title dispute was recently resolved at the Supreme Court of Spain level in Emerita’s favor: The project has been awarded to Emerita as the successful bidder. Emerita has received official notice from the Government of Huelva province awarding the public tender. The license has been issued and is posted on the official government website.

Excerpts from “Technical Report on the Iberian Belt West Project Exploration Concession“ (May 2021):

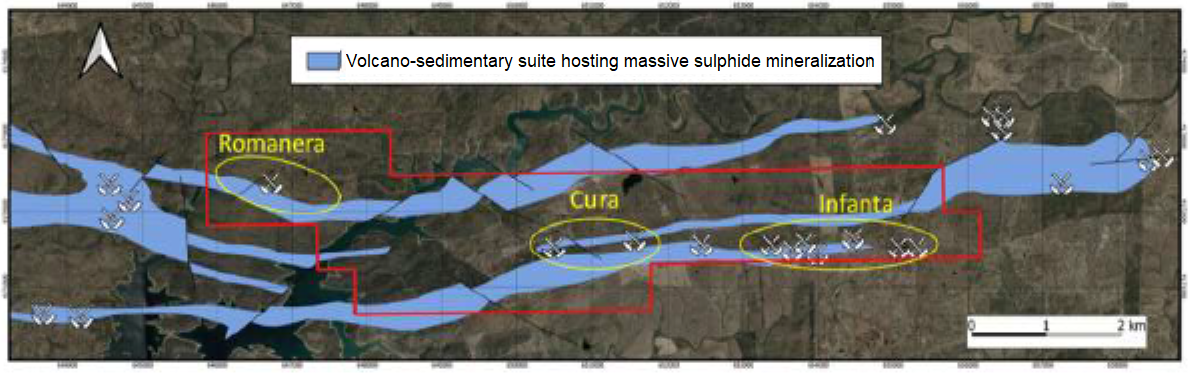

The Iberian Belt West (IBW) Project, previously known as ”La Romanera Project” hosts at least three volcanogenic, polymetallic sulfide mineral deposits, from west to east named “La Romanera”, “El Cura” and “La Infanta”.

Full size / La Romanera and La Infanta (spanish “infanta“, anglicised as “Infant“ or translated as “Princess“, is the title and rank given in the Iberian Kingdoms of Spain to the sons (“infantes“) and daughters (“infantas“) of the king) are two high-grade polymetallic VMS deposits (zinc-copper-lead-silver) extending from surface to shallow depths. Historical drilling intersected high grades but was limited by property boundary issues to approximately 120 m depth and 600 m strike. Emerita‘s ongoing drilling program aims to greatly increase the drilled area. The initial program is designed to test the depth extension to approximately 300 m (approximately 3x depth of present drill program) and evaluate the strike extent for in excess of 1.2 km. On July 20, 2021, Emerita announced to have mobilized a second drill rig at Infanta: “The initial drill program at Infanta is designed to test the full 1.2 kilometer strike length of the mineralization and test the depth extent to approximately 300 meters down dip. There are 49 historical holes drilled delineating the deposit to date and the program will move from the known mineralization and step out systematically along strike and down dip to establish a NI 43-101 compliant mineral resource estimate for the deposit. The plan will be to initially complete approximately 30 drill holes for a total of approximately 5,000 meters of drilling.“ (Source: Emerita Resources Corp.)

As a curiosity, it is believed that Balthasar, one of the three Wise Men and his present in gold came from this part Andalusia. They obtained gold, silver and copper from the “gossan”, the decomposed weathered sulphide material of reddish or rusty color that results from oxidized pyrites liberating particles of precious metals increasing its concentration on those at surface. Mineralization in the area has been known since Roman times due to the presence of its gossan surface expression and mined to some shallow extent on and off by different companies in the 19th and early 20th centuries. In the 1970s and 1980s major companies (Riotinto Minera SA, Asturiana de Zinc (AZSA), Phelps Dodge) explored the area, which at that time was broken into small mineral properties with different owners. For the first time ever, Emerita has a consolidated Property with the known mineral deposits within one exploration license.

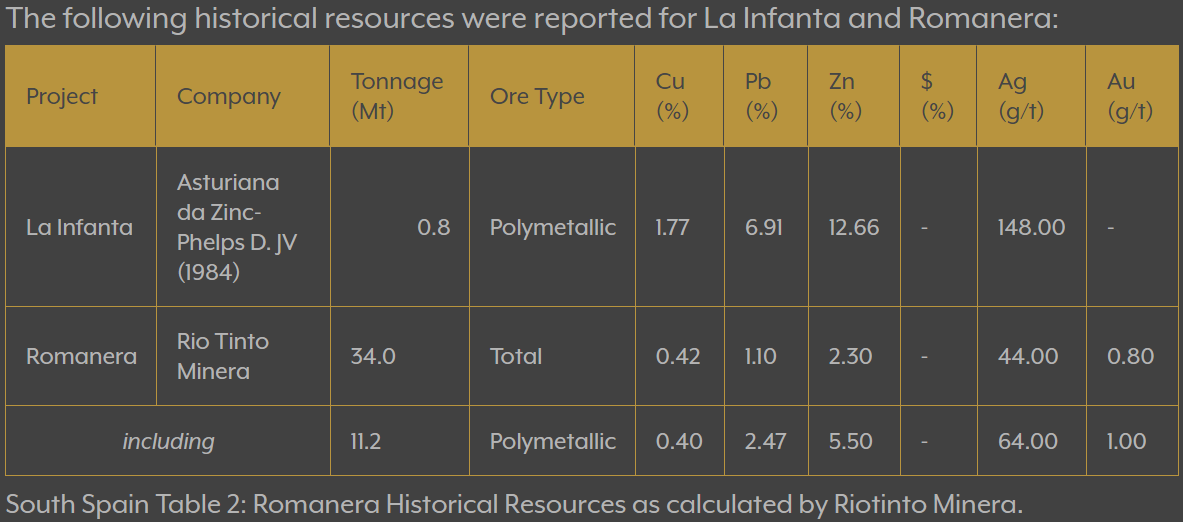

The Romanera deposit has produced minerals since Roman times, primarily from surface gossan material. In 1833 the deposit was bought by a small English company but there was low activity until 1907 when about 100 tonnes were extracted from a pit with 1.5% Cu. At that time the lenses were identified for a continuous length of 400 m at 50 m of depth and a thickness of 2 to 6 meters. In 1866, the French mining company La Huelvana mined 46 tonnes from trenches along the mineralized lenses... Historically, Romanera has over 20,000 metres of drilling done on the property and provides strong geological potential for growth... In the La Romanera deposit, during the 1960s, Asturiana de Zinc reported resources of 7.4 Mt from over 10,000 metres of DDH. In the same area, Rio Tinto Minera in the 1990s reported to contain 34 Mt of ore grading 0.42% copper, 2.20% lead, 2.3% zinc 44.4g/t silver and 0.8 g/t gold within which there is a higher grade resource of 11.21 Mt grading 0.40% copper, 2.47% lead, 5.50% zinc, 64.0 g/t silver and 1.0 g/t gold (Garcia-Cortes ed.,2011).

Full size / Romanera has a historical resource of 34 Mt at moderate grades including 11.2 Mt at high grades (J. M. Leistel, E. Marcoux, D. Thiéblemont, C. Quesada, A. Sánchez, G. R. Almodóvar, E. Pascual & R. Sáez, 1997). A Qualified Person, as defined in National Instrument 43-101, has not done sufficient work on behalf of Emerita to classify the historical estimates reported above as current mineral resources or mineral reserves and Emerita is not treating the historical estimate as current mineral resources or mineral reserves. The historical estimates should not be relied upon. (Source: Emerita Resources Corp.)

Full size / Romanera is a larger sulphide deposit which is located approximately 7 km to the west of La Infanta. During the 1960’s, Asturiana de Zinc explored the deposit which resulted in over 10,000 metres of DDH and 7.4Mt reported resources. Between 1990 and 1995, Rio Tinto Minera S.A. controlled most of the IBP, including La Romanera. In 2003, Matsa, Trafigura’s subsidiary in Spain acquired the “Aguas Tenidas” mine and acquired a large land position in the IBP which included the La Infanta and Romanera prospects. Matsa did not carry out exploration work on the property as it focused on the Aguas Tenidas mining operation. Historically, Romanera has over 20,000 metres of drilling done on the property and provides strong geological potential for growth. Romanera has a historical resource of 34Mt at moderate grades including 11.2Mt at high grades. Emerita has data for 51 drill holes on the Romanera Deposit, by Rio Tinto and certain holes by Asturiana. Asturiana did not assay for gold, certain holes will be redrilled. The mineralization remains open at depth for further expansion beyond the limits of the existing drilling. (Source)

Full size / Romanera is a larger sulphide deposit which is located approximately 7 km to the west of La Infanta. During the 1960’s, Asturiana de Zinc explored the deposit which resulted in over 10,000 metres of DDH and 7.4Mt reported resources. Between 1990 and 1995, Rio Tinto Minera S.A. controlled most of the IBP, including La Romanera. In 2003, Matsa, Trafigura’s subsidiary in Spain acquired the “Aguas Tenidas” mine and acquired a large land position in the IBP which included the La Infanta and Romanera prospects. Matsa did not carry out exploration work on the property as it focused on the Aguas Tenidas mining operation. Historically, Romanera has over 20,000 metres of drilling done on the property and provides strong geological potential for growth. Romanera has a historical resource of 34Mt at moderate grades including 11.2Mt at high grades. Emerita has data for 51 drill holes on the Romanera Deposit, by Rio Tinto and certain holes by Asturiana. Asturiana did not assay for gold, certain holes will be redrilled. The mineralization remains open at depth for further expansion beyond the limits of the existing drilling. (Source)

The Infanta deposit produced 400 tonnes between 1890 and 1895. A shaft of 40 meters deep connected to two parallel mining levels 15 m apart of 10 to 15 meters long. No other production is known from La Infanta deposit... In the La Infanta deposit, AZSA estimated resources of 1 Mt at high grades based on a drill campaign over 5,000m (Leistel, 1998)... In 1975, Asturiana de Zinc S.A. acquired the exploration rights and signed a JV agreement with Phelps Dodge Española, S.A.

Phelps Dodge kept the project and completed a feasibility study to ship the ore to “Cueva de La Mora” mine, about 30 km to the north. The project was never implemented, and in the late 1990’s, the exploration licenses returned to the state as “strategic resources”. La Infanta has over 5,000m of drilling done on the property with historical resources of 2Mt at very high grades. The project provides for high geological potential for growth with low environmental risk. La Infanta has provided very high grade intercepts and is only drilled to approximately 100 metres depth.

Full size / Just like Romanera, Infanta is a polymetallic VMS deposits (zinc-copper-lead-silver) extending from surface to shallow depths. Historical drilling intersected high grades but was limited by property boundary issues to approximately 120 m depth and 600 m strike. At Infanta, the massive sulfide lens has a strike length of over 800 m and averages about 1.5 m in thickness and the total mineralized horizon averages about 4 m... The mineralization of the Infanta area consists of high-grade, massive sulfides with associated lower grade disseminated and brecciated ore (the low-grade term is very relative because when the description was done 6.0-10% base metal was considered low grade in the context of this zone). The massive sulfide mineralization is high-grade and averages near 50% combined base metals. The massive sulfides are fine-grained sphalerite, galena, chalcopyrite and tetrahedrite with only minor amounts of pyrite. The mineralization is fine-grained with 10-15% of the grains measuring less than 40 microns. (Source)

The Cura deposit, located on the left bank of the River Malagón, and in the middle of the other two deposits had a separate history; it also shows shallow workings from roman times. After a long period of inactivity and according to the mining engineer and writer Gonzalo Tarin (1886) towards the end of the 19th century, some old shafts were explored and a 1.25m wide intersection of sulfide mineralization rich in copper, lead and silver was found. The mining group sold the tenements in 1872 to the Malagón Mines Company, which after producing about 300 tons, abandoned the tenements. Some exploration took place in 1938 and 1943. Phelps Dodge explored the deposit in 1975 and 1985... At El Cura there is an estimate of 1Mt @ 1.85%Cu, 2.0% Pb, 4% Zn (Geode conclusions)... The Company [Emerita] has little information about the Cura deposit, other than it is stratiform based on mapping, and that it was mined in the past. Disseminated mineralization towards the south suggests that the remains of the deposit may be of a similar character to Infanta... In El Cura deposit an adit from the 19th century of less than 100 meters, presumably to intercept the mineralized lenses, is known to be buried. There is also a 60 m deep shaft, that intercepts two mineralized lenses 900 m apart, at 47 m depth. Another shaft, to the west also intercepted a lens. In 1946, the explorer Pinedo Vara found a pile of ore with the following grades 5.7 % Cu, 14.0 % Pb, 24.0 % Zn, 2.0 % Sb, and 580 g/t Ag. According to the same source, the deposit was not considered economic at the time despite the high metal content, due to metallurgical problems for copper and lead smelters of the day...

From the 19th century until the 1980s different companies over different periods have conducted exploration and/or mining works in the area where the IBW project is located. The most relevant exploration was carried out by three companies: Asturiana de Zinc, Phelps Dodge and Rio Tinto. The three companies explored the area at the same time during the 1980s and 1990s, competing also for the mine properties, which was divided in numerous mineral claims. The exploration consisted in geochem sampling, geological mapping at different scales, geophysical surveys and diamond drilling.

Between 1960-1977 Asturiana de Zinc (AZSA) owned La Romanera and in 1975 also acquired Infanta in JV with Phelps Dodge Española SA. In 1975 Phelps Dodge also explored El Cura deposit.

Between 1990 and 1995 the Spanish company Rio Tinto Minera S.A. controlled most of the IPB, including La Romanera.

In 2003 Matsa, Trafigura’s subsidiary in Spain acquired the “Aguas Teñidas” mine and acquired a large land portion in the IPB which included the La Infanta and Romanera prospects. Matsa did not carry out exploration work on the property as it focused on the Aguas Teñidas mining operation.

On December 5, 2013, the Andalusian Government, through its Director of Industry, Energy and Mines Bureau, released for public bidding all exploration permits that, for different administrative reasons, had lapsed in Andalusia.

After an extensive review of mineral opportunities in Spain, Emerita-E participated in the public tender for lapsed exploration permits in Andalusia, in the Huelva province. This public tender was announced on November 25th, 2013 by the Delegation of Huelva. The tender consisted in several old exploration permits, enclosing mineral deposits and occurrences that were explored in the early 1980s by major companies. It was a requirement of the bidding process to demonstrate sufficient financial capability and proven technical expertise in conducting exploration programs. Emerita-E prepared the application, which included an exploration program that was submitted to the Mines Department for its consideration.

The tender was resolved in favor of another bidder on June 25th, 2014. Emerita-E considered its bid was not assessed fairly and appealed the resolution.

On September 19, 2017, the High Court of Justice of Andalucía partially upheld the appeal of Emerita-E, ordering a new evaluation in terms that were beneficial to Emerita-E. The Regional Government of Andalusia brought an appeal in cassation before the Supreme Court of Spain.

On October 22, 2019 the Supreme Court of Spain confirmed the ruling supporting Emerita-E‘s Challenge to the IBW Project (La Romanera) Tender Award.

On September 1, 2020, Emerita-E was officially notified through a resolution that it was the winning bidder of La Romanera mining rights in Huelva province. The permit which occupies 51 claims equivalent to an area of 1530 Ha... The exploration concession was granted to Emerita-E in September, 2020, for a period of 26 months with the option to renew. The exploration period commences when the granting process is completed.

According to the European regulations there are no mining royalties, taxes or administrative liabilities associated to the exploration concession. The corporate rate of income tax in Spain is 25%, and value added tax is 21%.

There is excellent access and infrastructure into and on the Property, and though the region has a history of mining, it has seen little in the way of modern exploration.

Modern Exploration

Last week (August 13, 2021), Emerita announced initial results from the ongoing phase-1 drilling program at Infanta (IBW Project), where a second drill rig was added in late July 2021 and a third drill rig is planned to be added once drilling starts on the Romanera and/or Cura deposits.

Excerpts from Emerita‘s news-release “Emerita Reports High Grade Assays From Initial Drill Holes On La Infanta Drill Program“ (August 13, 2021):

Emerita Resources Corp. (TSX – V: EMO; OTC: EMOTF) (the “Company” or “Emerita”) announces that it has received complete assays for the first two drill holes from the Infanta drill program. Additional assays are expected in the coming week and it is expected there should be a steady flow of new assay data as drill holes are completed going forward.

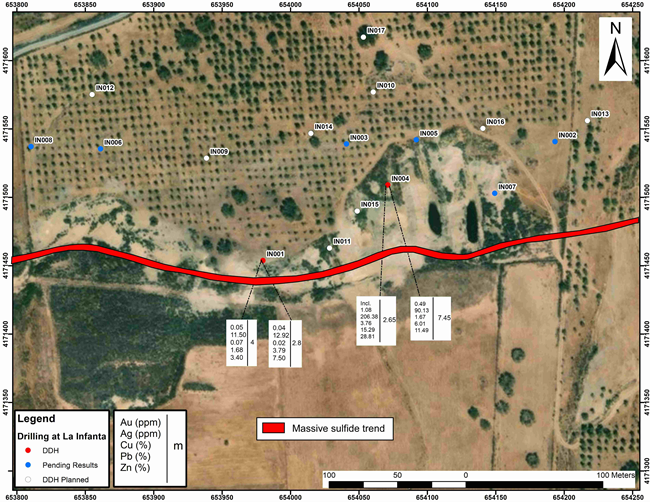

There are presently six drill holes in the process of being assayed. Emerita has added a second diamond drill which is expediting the drilling of the La Infanta deposit. Please see Figure 1 below for drill hole locations and Table 1 below for assays and drill hole coordinates. The holes are located approximately 100 meters apart along strike.

Full size / Table 1 from Emerita‘s news-release on August 13, 2021

• Drill hole IN004 intersected 7.45 meters grading 1.67% copper, 6.01% lead, 11.49% zinc and 90.1 g/t silver and 0.49 g/t gold from 62.55 meters, including 3.76% copper, 15.29% lead, 28.81% zinc and 206.3 g/t silver and 1.08 g/t gold over 2.65 meters from 64.55 meters depth (see cross section - Figure 2).

• Drill Hole IN001intersected 4.0 meters grading 0.07% % copper, 1.68% lead, 3.40% zinc and 11.50 g/t silver from 24.3 meters, and a second intercept of 2.8 m grading 0.02 % copper, 3.79% lead, 7.50% zinc and 12.95 g/t silver from 32.3 meters depth (see cross section – Figure 3). This hole is near surface and likely suffered some leaching of the mineralization related to surface weathering as it is only approximately 15 meters vertically from surface.

• Intersection widths are expected to be approximately true width. Assays were conducted at ALS Laboratories, a certified independent assay lab.

Full size / Figure 1 from Emerita‘s news-release on August 13, 2021

Full size / Figure 2 from Emerita‘s news-release on August 13, 2021

Full size / Figure 3 from Emerita‘s news-release on August 13, 2021: “Section showing hole IN001. It is likely that the mineralization in this hole was impacted by partial leaching due to surface weathering processes as it is at a vertical depth of approximately 15 meters, suggested by uncharacteristically low values particularly for silver. The hole intersected two zones separated by a more weakly mineralized interval. The entire interval from 24.3 meters to 35.1 meters grades 3.51% zinc, 1.76% lead over 10.8 meters...“

According to Joaquin Merino, P.Geo., President of the Company: “It’s a very exciting time to be working in our core shack. With two drills operating now, we are seeing a steady supply of new drill core and are awaiting every batch of assays with anticipation. These are the first two holes for which we have complete assays, however all drill holes to date have well mineralized intervals that are now in the pipeline for assays. We are systematically stepping out through the deposit to build the geological model that will meet the requirements for establishing a NI 43-101 compliant mineral resource estimate.”

The initial drill program at Infanta is designed to test the full 1.2 kilometer strike length of the mineralization and test the depth extent to at least 300 meters down dip. Our ongoing geological mapping confirms there is solid evidence, including some historical excavations, that mineralization should persist over that strike length and this is further supported by the preliminary results of the ongoing geophysical survey, which also suggests the mineralization continues to depth below the historical drilling. There are 49 historical holes delineating the deposit to date and the program is moving from the known mineralization and stepping out systematically along strike and down dip to establish a NI 43-101 compliant mineral resource estimate for the deposit.

David Gower, P.Geo., Emerita’s CEO noted, “This is just the beginning of this project. The team is excited by what we are seeing in the core shack. The ongoing EM survey (see News release dated July 20, 2021) is providing excellent information that will be valuable in targeting drill holes and data suggests the deposits continue at depth well beyond present drilling. The Company will add a third drill rig once we commence drilling on the Romanera and/or El Cura deposits.”

Health and Safety

Company employees and contractors continue to follow all protocols related to COVID 19 precautions required to safely operate safely. Summer temperatures in this area get very hot and for safety reasons the Company does not operate the drill rigs when temperatures exceed 40 degrees centigrade.

Qualified Person

The scientific and technical information in this news release has been reviewed and approved by Mr. Joaquin Merino, P.Geo, President of the Company and a Qualified Person as defined by National Instrument 43-101 of the Canadian Securities Administrators.

This press release contains “forward-looking information” within the meaning of applicable Canadian securities legislation. Forward-looking information includes, without limitation, statements the mineralization of the Iberia Belt West Project (the “Project”) including the infanta deposit, the prospectivity of the Project, the timing and results of the drill program, the Company’s ability to complete a NI 43-101 compliant resource estimate, the impact of changes in the mining laws and regulations, the impact of COVID 19 and the Company’s future plans. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”. Forward- looking information is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Emerita, as the case may be, to be materially different from those expressed or implied by such forward-looking information, including but not limited to: general business, economic, competitive, geopolitical and social uncertainties; the actual results of current exploration activities; risks associated with operation in foreign jurisdictions; ability to successfully integrate the purchased properties; foreign operations risks; and other risks inherent in the mining industry. Although Emerita has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking information. Emerita does not undertake to update any forward-looking information, except in accordance with applicable securities laws.

Aznalcóllar – Los Frailes

The Aznalcóllar Zinc-Lead-Copper-Silver Project includes 2 past producing open-pit mines: Aznalcóllar (“Corta Aznalcóllar“, 1975-1996) and Los Frailes (“Corta Los Frailes“; 1995-2001), the latter closed due to a combination of low zinc prices and a severe tailings damn failure (1997). The operator at that time, Swedish mining giant Boliden, and the government subsequently rehabilitated the site. Boliden ultimately left Spain, returning the project to the Spanish government. Due to demands of the local community for employment, the government initiated a public tender to re-develop the mine. The tender was unanimously supported by all political parties.

Full size / Corta Aznalcóllar: “This pit was mined from October 1975 to June 1996... After mineral extraction was completed, it was used as a dump for the neighbouring Los Frailes pit. It then became a deposit for the sludge collected during the cleaning of the Guadiamar river after the dam was broken up in 1998, and has subsequently received materials from the cleaning of some low-grade stocks and has also been used as part of the water purification circuit prior to discharge into the river. It is currently partially filled with contact water, tailings and low-grade materials from Los Frailes and sludge from the cleaning of the tailings dam break.“ (Source)

Full size / Corta Los Frailes: “After the end of ore mining at the Aznalcóllar mine, the Los Frailes mine was opened in September 1995 and remained in operation until 2001, when mining activity ceased definitively due to the fall in the price of metals. The cessation of operations at the Los Frailes pit occurred without completing the extraction of ore from the deposit, which is currently flooded with runoff and rainwater. Precisely because it was operated earlier, some of the necessary infrastructure and facilities are already in place, which means that less time is needed for the start of operations.“ (Source)

In 2014, Emerita participated in the tender process, which was run in 2 stages: The first was a financial qualifying round, whereafter Emerita and Minorbis were the only companies qualified for the second round, which required a detailed technical plan for the development of the project. Emerita completed a full mine plan, environmental management plan, water management plan (which the Federal Water Authorities endorsed), and public hearings in the community. Emerita has spent ~$1 million on engineering studies and other documentation (almost 10,000 pages) in regards of the project tender.

In 2015, the tender was awarded by a very slim margin: Minorbis’ bid was chosen as the winner. Upon examining the details, Emerita challenged the decision and filed charges of corruption against the panel. As per Spanish law, if there is a commission of a crime in a public tender process, the award must be negated and the tender goes to the next qualified bidder. As Emerita believes to be the only other qualified bidder, the company hopes to be on the verge of being officially awarded the project.

Emerita‘s President, Joaquin Merino (P.Geo), noted in July 2021: “We are entering the final stage of this legal odyssey. The years of investigations have been concluded, the crimes are serious, the judge is expected to set a trial date in the near future and based on the evidence and numerous decisions by the Spanish courts to date we are confident that the accused will be found guilty of one or more crimes.” Emerita’s CEO, David Gower (P.Geo), added: “This is an important outcome with respect to the Aznalcollar trial and by extension the ultimate awarding of the public tender. Emerita is well positioned to begin immediately developing this tier 1 asset for the benefit of the community and all stakeholders. This final ruling by Court No. 3 of Seville brings all levels of the judiciary that have been involved in the hearings over the past seven years into alignment and agreement on the charges for the commission of criminal acts related to the awarding of the public tender. Importantly, it also makes it clear that the other bid should have been disqualified from the process as demonstrated by the fact that a number of the charges stem from the fact that it was permitted to proceed even though it did not meet the criteria required by the tender instructions. Considering this, Emerita is the only qualified bidder. This brings the process a step closer to a conclusion. According to legal counsel in Spain it is very rare for a trial to proceed to this final stage in Spain that does not conclude with conviction(s). Counsel also advises that this phase is generally not a long, protracted process as the investigation is closed and no further evidence can be submitted and appeals to delay the process are no longer permitted.”

Full size / The tailings ponds at the Aznalcóllar Mines site are tremendous in size due to operation of a large open-pit mine (Los Frailes) and can be reduced significantly with underground mining, minimizing the risk of future dam failures. Boliden’s mine plan for Los Frailes included a low-grade but large open-pit with a historical resource estimate* of 71 Mt @ 3.86% Zn, 2.18% Pb, 0.34% Cu + 60 g/t Ag. Emerita‘s review of the historical drilling data indicates the potential existence of a higher grade portion of the resource that is estimated* to contain 20 Mt @ 6.65% Zn, 3.87% Pb, 0.29% Cu + 84 g/t Ag (“remains open for expansion“). In its documentation filed for the public tender process, Emerita proposed to first mine the higher grade portion of the deposit with underground methods. Benefits: No huge waste rock piles and tailings ponds, tailings go back underground as paste fill, lower capital expenditures, smaller mill.

Full size / The 20 Mt high-grade portion of the historical resource* is entirely within the Los Frailes Deposit (center), the past producing Aznalcóllar Deposit (right) and a third deposit also “remain open and provide upside“. Deposit outcrops in the open pit and remains open at shallow depths. The deposit thickness ranges between 30 and 90 m. The thickest section of the ore body lies below 150 m depth from surface. The Los Frailes and the previously mined Aznalcóllar deposits are both open for further expansion by drilling at depth, as historical drilling was primarily constrained to depths accessible by open pit mining. (Source) *A qualified person as defined in NI 43-101 has not done sufficient work on behalf of EMO to classify the historical estimate as a current mineral resource and EMO is not treating the historical estimate as current mineral resource or mineralreserve. The resource estimate is a historical estimate and should not be relied upon. Significant additional drilling and related work would be required to make the estimate a current mineral resource under NI 43-101. A summary of thehistorical resource estimate is available on the Government of Andalucia’s website in a report prepared by the prior operator of the Aznalcóllar Project entitled “Proyecto de Explotacion Yacimiento Los Frailes, Memoria Andaluza de Piritas, Boliden-Apirsa, Octubre 1994” (Los Frailes Development project Report, Boliden-Apirsa, October 1994) along with subsequent resource estimate updates, the latest being from 2000. (Source)

The past producing Aznalcóllar Mines (Minas de Aznalcóllar) are located near the town of Aznalcóllar at the eastern end of the Iberian Pyrite Belt in southwestern Spain (Huelva Province, Andalucia Region) and approximately 40 km west of the large city of Sevilla. The Aznalcóllar Mines are located between 2 other major metal mining deposits: Cobre Las Cruces, located 10 km away, which is in the operational phase; and Riotinto, 50 km away, which is also producing from an open pit.

“The Aznalcóllar orebody was discovered in 1956 and brought into production in 1979 by Andaluza de Piritas, S.A. (Apirsa) owned by Banco Central S.A. (Eptisa, 1998). Boliden purchased Apirsa in 1987. A second orebody, named Los Frailes with more than 70 Mt of ore, was then discovered and was mined shortly after.“ (Source)

Excerpts from a dossier by the Junta de Andalucia (2014; freely translated from Spanish):

For the opening of the Los Frailes Mine in 1995, initial resources were estimated at 71 Mt averaging 0.34% Cu, 2.18% Pb and 3.86% Zn, 60 ppm [60 g/t] Ag (Source: Boliden Apirsa, S.L.). The economic reserves estimated by Boliden Apirsa, S.L. for the opening of this mine were some 47.37 Mt averaging 0.35% Cu, 2.17% Pb and 3.82% Zn, 60 ppm Ag.

Excerpts from Boliden‘s Annual Report (1997):

Attainment of full production at Boliden Apirsa’s Los Frailes zinc mine in southern Spain was the single most important achievement in the Company’s mining operations in 1997. The open pit mine began production in early 1997 and by year end reached its planned annual ore production rate of 4 million tonnes. Los Frailes is expected to produce 125,000 tonnes of zinc in concentrate in 1998 as well as 4,700 tonnes of copper, 48,000 tonnes of lead,and 3 million ounces of silver in concentrates. Los Frailes is adjacent to the depleted Aznalcóllar zinc mine, about 45 km west of Seville. Boliden closed the Aznalcóllar mine in late 1996 after19 years of operation, and is using much of the existing infrastructure for the Los Frailes operation.

To process the increased mine output of the Los Frailes mine, the existing concentrator capacity was expanded to 4.0 million tonnes from 2.3 million tonnes and will be further expanded to 4.2 million tonnes by 2000. Significant modifications to the mill include the introduction of fully autogenous grinding and the installation of larger, 100-cubic-met reflotation cells. Total capital cost of the Los Frailes mine and concentrator expansion was $US167 million.

Full size / “The news of the tailings disaster led to a 28 percent decrease in the value of Boliden in the Toronto stock exchange in the space of five days. The financial markets were said to be ‘punishing’ Boliden for the disaster and its statement of waiting until the courts decided to pay compensation. Boliden later launched an information campaign through the internet about it cleaning up to which the markets reacted well and the share value increased by 4.92 percent. The share value price reached a bottom of $9.05 and recuperated up to $9.60. Their highest value had been $12.45 days before the incident.“ (Source / Image)

Excerpt from Boliden‘s Annual Report (1998):

In Spain, the Los Frailes zinc mine owned by our subsidiary, Boliden Apirsa SL (Apirsa), reached its design capacity in the fourth quarter of 1997. Los Frailes has the capacity to process four million tonnes of ore, producing about 125,000 tonnes of zinc and three million ounces of silver per year. Operations proceeded according to plan in the first quarter of1998. However, on April 25, 1998, a failure in the tailings dam at the mine resulted in the release of tailings and tailings water into the nearby Agrio and Guadiamar river channels and surrounding areas. Operations were immediately suspended.

Excerpts from “The 1998 dam breach at the Los Frailes mine in Spain“ (Boliden):

In April 1998, a dam breach accident occurred in the tailings pond at the Los Frailes mine in Spain, which was then owned by Boliden‘s subsidiary, Boliden Apirsa S.L. (“Apirsa“). Boliden is involved in a number of disputes and legal proceedings arising from the accident at the mine...

Mining operations were halted immediately and all available in-house resources were mobilised to clean up the affected area, to limit the damage done, and to restore the natural landscape. The area was cleaned up by Apirsa in collaboration with the central government and the local government (Junta de Andalucía). The three parties took an immediate decision whereby they would each clean one third of the area. Apirsa undertook to take the area closest to the mine (0-12 km) where approximately 70-80 per cent of the tailings sand had been deposited. No agreement was reached regarding the costs of the clean-up. By the end of 1998, the major part of the area had been cleaned up. Apirsa‘s total costs in respect of the dam breach accident were approximately EUR 115 million.

Production restarted at the mine in 1999, but the accident resulted in increased production costs and other operational problems which, in combination with low metal prices, resulted in the mining operations being terminated after two years and Apirsa applying for a „suspensión de pagos“, a form of composition proceedings. The composition agreement was reached in October 2002, when more than 250 creditors were paid in accordance with the agreement.

The Los Frailes mine is now owned by the local government and Apirsa is subject to liquidation proceedings since 2005, by its own initiative. Following the dam breach the prosecutor initiated a criminal investigation and it was determined that the accident was caused by design and construction errors in the dam, not by Apirsa‘s handling of the operations at the mine. There was no suspicion of crime and the prosecutor did not bring charges against Apirsa. In 2002, following the result of the criminal investigation, Apirsa initiated an action for damages against the companies responsible for the dam‘s design and construction, and their insurance companies. However, the Spanish Supreme Court rejected in final Apirsa‘s claim in January 2012.

The Spanish Ministry of the Environment submitted a claim against Apirsa to pay approximately EUR 45 million. The claim was affirmed in the highest instance in 2004 and Apirsa was ordered to pay approximately EUR 45 million in respect of the authorities‘ clean-up costs, and of damages and fines. This resulted, in January 2005, in Apirsa initiating insolvency proceedings in order to ensure a coordinated and orderly closure of the company...

Junta de Andalucía is claiming compensation both from Boliden Apirsa S.L. which, at the time of the accident, owned and operated the mine and which is subject to liquidation proceedings since 2005, and from Boliden BV and Boliden AB in their capacities as direct and indirect owners of Boliden Apirsa S.L.

Full size / View of the Aznalcóllar‘s eastern dump, from the re-industrialized area. (Source)

Full size / View of Aznalcóllar‘s former industrial area (“Mineralogical Plant“), run-off ponds and the restored tailings dam in the background (used for processing material from Los Frailes; Source)