Full size / Fluorite from the USA (Source: Mindat.org)

Disseminated on behalf of Ares Strategic Mining Inc. and Zimtu Capital Corp.

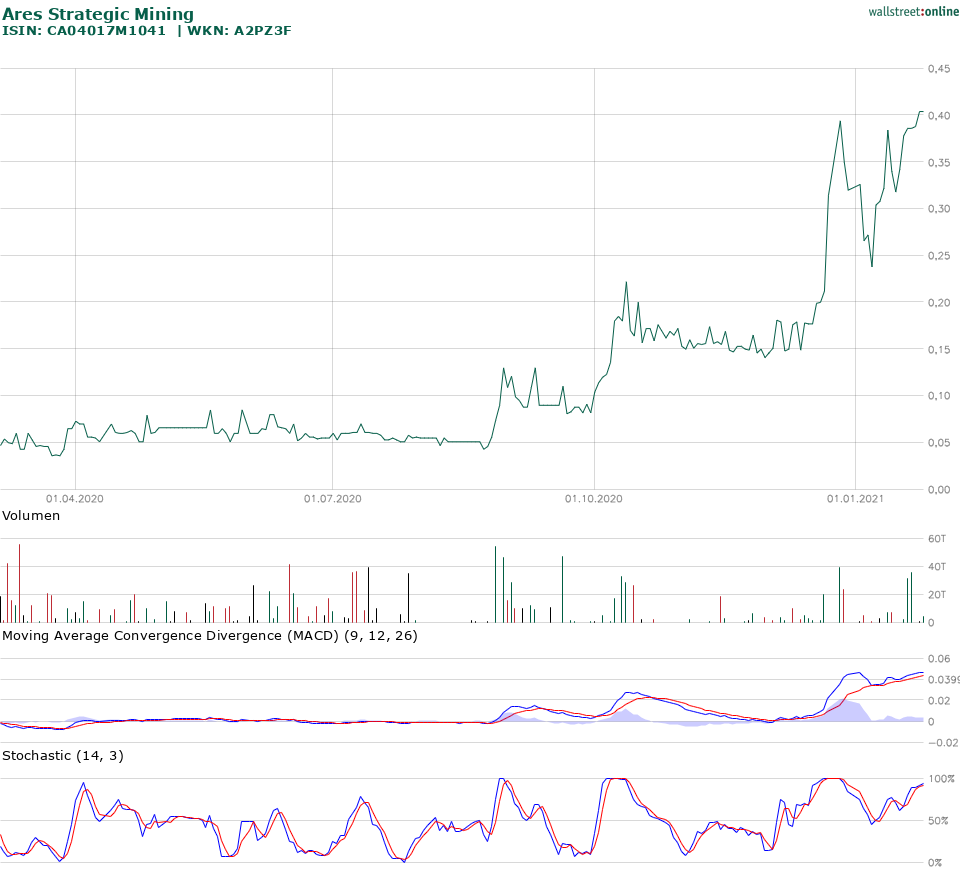

Before Ares Strategic Mining Inc. released assays from its maiden drilling program at its 100% owned Lost Sheep Project in Utah last year in August, its share prices traded at the $0.10-level on the Canadian TSX Venture Exchange. Backed by a strong newsflow over the last months, its share price closed at $0.60 yesterday. Today, Ares released long-awaited assays from its phase-2 drill program to delineate additional mining targets, with the result of “Greater mineralized fluorspar widths and consistent grades compared with first drill program“. Based on today‘s assays, “Ares can now complete its mine plan and engineering work to progress into the construction phase of the project“.

Ares also stated in today‘s news:

• “Ares discovers large high-grade fluorspar mineralization, at least 60 m down plunge, averaging over 80% pure fluorspar, and is still open at depth.

• Large fluorspar mineralized zones found at surface, averaging over 50% fluorspar.

• High-grade veins found between fluorspar pipes.

• Every drill hole intersected fluorspar during this exploration program.“

With these results, “Ares has successfully located and confirmed additional fluorspar mineralization within its permitted mining area, which will be included in its primary mining operation for 2021“.

With fluorspar being one of the most critically important commodities for industrial and economic growth in the US, Ares is uniquely positioned to assist the nation in breaking free from its foreign dependency on fluorspar supply.

James Walker, Ares‘ President and CEO, commented in today‘s news: “We are pleased to have received these long-awaited assay results and are excited to complete our mine planning and advance the operation. We knew from visual confirmation that the quality of fluorspar from the drill program was high, and its great to have the laboratory confirm these estimations. The assay results can now be fitted to a block model, and the optimum mining methods can be finalized. Ares continues to demonstrate some of the highest naturally occurring grades of fluorspar in the world, while concurrently demonstrating negligible detrimental impurities. Combined with Ares’ recent metallurgical advancements, the prospects of the expanded mining operation continue to improve.”

Click below or here to watch today’s video news-release with CEO James Walker discussing the significance of today’s news:

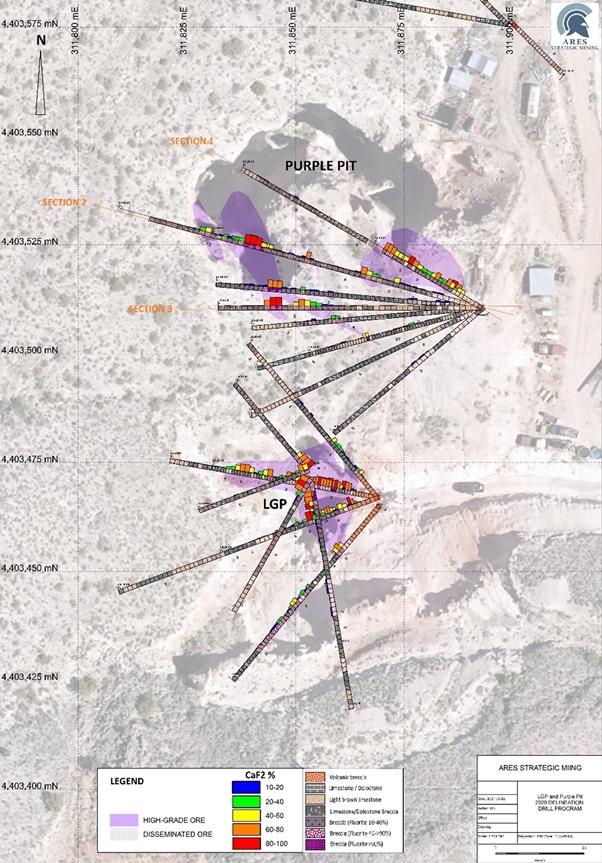

According to the news: “A total of 10 reverse circulation drill holes, drilling approximately 875 meters, were collared between the two known fluorspar deposits on the Company’s permitted mining area. Fluorspar mineralization was consistent throughout the entire area, connecting the large fluorspar deposits examined during two previous drill programs in 2020. Drilling was directed under the shallower part of the Purple Pit, where large areas of unmined fluorspar mineralization were intersected, proving an additional 60 m of high-grade fluorspar (see Figures 2, 3 and 4). These fluorspar pipes remain open at depth.“

Figure 1: Drill hole plan section outlining the distribution of fluorspar mineralization.

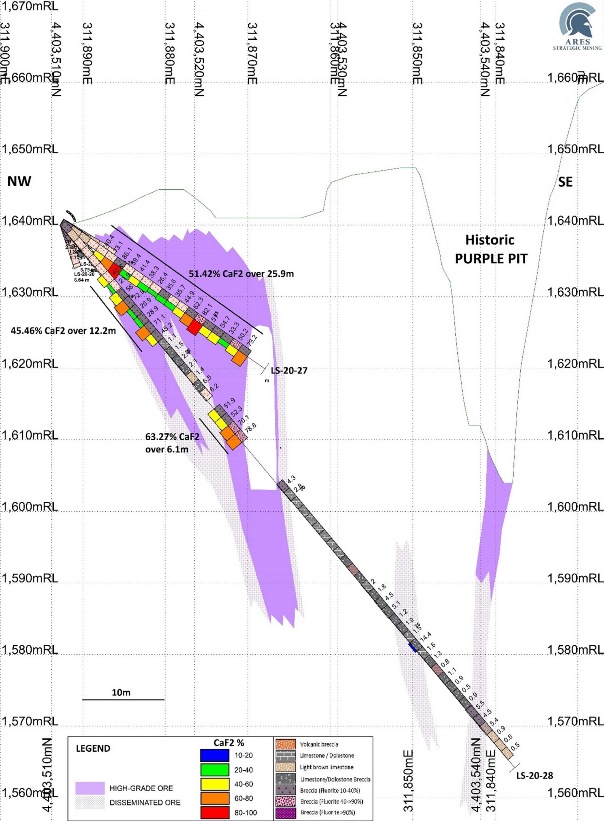

Figure 2: Drill hole section 1 (LS-20-27 and LS-20-28) outlining the distribution of fluorspar mineralization.

“Drill Holes LS-20-27 and LS-20-28 intersected a very shallow zone of fluorspar mineralization at surface, that extends 20m x 10m in plan view and 30m down dip (See figure 2).”

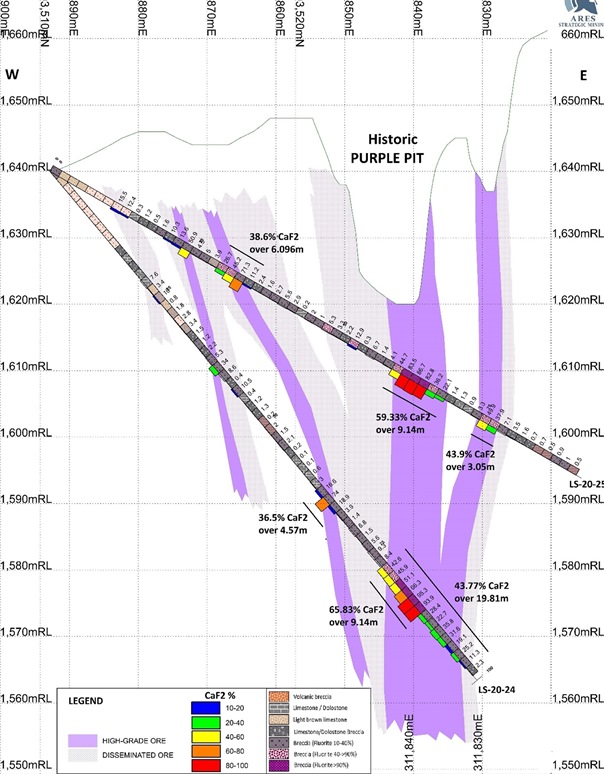

Figure 3: Drill hole section 2 (LS-20-24 and LS-20-25) outlining the distribution of fluorspar mineralization.

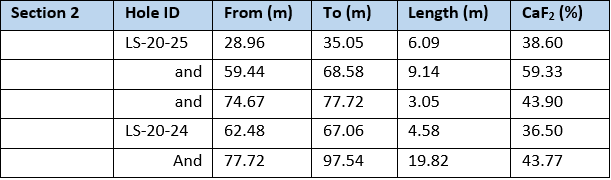

“Drill holes LS-20-24 and LS-20-25 (Section 2) test the down dip projection of the fluorspar mineralization left at the bottom of the Purple Pit and successfully intercepted mineralization over 50 meters beneath the historic pit floor. The zone remains open at depth. In this section the main pipe appears to split into two zones, indicating a smaller pod to the west of the main pipe that intersected 3.05 m of 43.9% CaF2 from 74.67 to 77.72m. Drill hole LS-20-25 also intersected fluorspar mineralization in the main pipe that returned 59.33% CaF2 over 9.14 m from 59.44 to 68.58 m down hole, including a high grade zone at 60.96 to 65.53 m down hole (4.57 m of 84.33% CaF2). Drill hole LS-20-24 undercut LS-20-25 and intersected the main mineralized below the Purple Pit returning 43.77% over 19.81 m from 77.72 to 97.54 m down hole (including a high grade sub-interval of 3.05 m of 94.58% CaF2 from 83.82 to 86.87 m down hole). The upper part of hole LS-20-24 intersected a thin zone of fluorite mineralization also found in drill holes LS-20-27 and LS-20-28, and returned 4.57 m of 36.50% CaF2 from 62.48 to 67.06 m down hole.” (See figure 3)

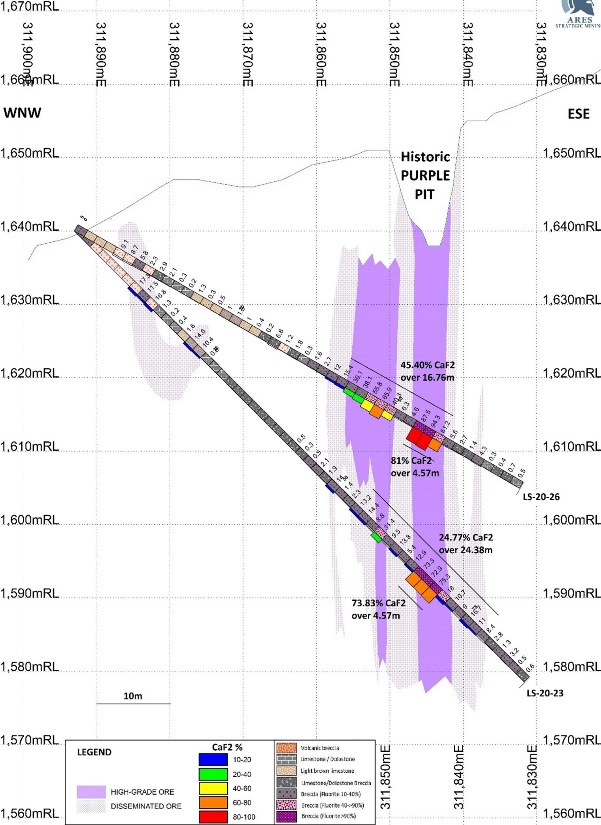

Figure 4: Drill hole section 3 (LS-20-23 and LS-20-26) outlining the distribution of fluorspar mineralization.

“Drill holes LS-20-23 and LS-20-26 (Section 3) also show over a 50 meters extension of fluorspar mineralization from the Purple Pit floor and mineralization remains open at depth.” (See figure 4) “Fluorspar mineralization is very homogeneous in both the upper intersect in hole LS-20-26 from 41.15 to 57.91 m down hole averaging 45.40% CaF2 over 16.76 m (including 4.57 m of 81% CaF2). Drill hole LS-20-23 undercut the previous hole and intersected strong fluorspar mineralization from 53.34 to 77.72 m down hole averaging 24.77% CaF2 over 24.4 m, including a high-grade interval of 4.57 m of 73.83% CaF2. The true width of the fluorspar mineralization in these areas range between 10 and 15 meters.”

The results reported are intersect lengths and due to the nature of the fluorspar mineralization as irregular breccia pipes they are not considered true widths at this moment. Assay method for CaF2 consisted of 201-676 Lithium Borate Fusion, Summation of Oxides and XRF Finish. Routine blank, standard, and field duplicates were inserted in the sample batches following standard QA/QC practices. Raul Sanabria, P.Geo., is a qualified person as defined by NI 43-101 and has reviewed and approved the technical contents of this news release. Mr. Sanabria is not independent to the Company as he is a Director and shareholder.

Assays from the phase-1 drill program (August 2020): See here

Click below or here to view a 3D model of the fluorspar distribution and drill hole intersects (August 2020):

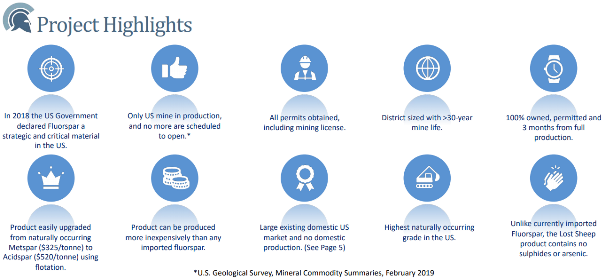

Ares‘ Lost Sheep property includes the only permitted fluorspar mining operation in the US, which produced insignificant fluorspar quantities until Ares took over in early 2020. The property was never mined by a big mining company, only artisanal and small-scale mining of high-grade fluorite (metspar quality) at surface, supplying small shipments to steel producers. There was never any systematic exploration and mining until Ares started a drill program and working professionally with the goal of expanding production. The mine site is currently equipped with extraction equipment adequate for continuing a small-scale operation (in place prior to Ares taking over). Additional equipment and upgrades are necessary in order to scale operations (Ares announced a $10 million USD lease financing for its plant and equipment purchases on November 4, 2020). The property benefits from excellent access with paved highway to the site because there is a near-by berrylium mine (used in nuclear) maintained by the government. The mine site is 72 km northwest of Delta, Utah, where Ares also owns a warehouse and packing facility, attached to a railway network. (Images from Ares)

On January 19, 2021, Ares announced that its “metallurgists and process engineers have greatly improved both grades and recoveries during on-going metallurgical work“, achieving “99.9% pure fluorspar [acidspar] and 92% recoveries for high-grade metspars“:

“The Company has been continuously refining its flotation and upgrading processes, and its flotation expertise ever since achieving its desired product of acidspar. Acidspar is a 97% CaF2 (fluorspar) product which comprises almost 70% of the fluorspar market. Acidspar is required for aluminum manufacture, fluorine for medical ingredients, refrigeration units, Teflon, hydrofluoric acid, and electronics. Through continued work the Company has refined its metallurgy and processing, to achieve an almost completely pure CaF2 product from its raw fluorspar taken from its Utah mine.“

“Additionally, the Company has been working to improve the amount of material recovered during its upgrading process. Through a combination of adjusted reagent levels, float times, grind size, and collectors, the Company has determined the best methodologies for its particular fluorspar deposit and has achieved over 92% recoveries when manufacturing its high grade metspar – another fluorspar product. Metspar is used in the manufacture of steel, ceramics, fiberglass, and assists with desulfurization and dephosphorization during smelting processes to enhance the tensile strength of forged metals. A metspar product of over 90% CaF2 is considered high-grade, and commands higher selling prices than more common metspars. The Company’s metallurgists have produced a 93% pure metspar from its naturally occurring fluorspar, while only losing 8% during the flotation process. These advances act to greatly increase both the output and value of the Company’s planned industrial products.“

“Fluorspar’s classification as a Critical Mineral in the United States translates to a faster permitting period, enabling mining operations to initiate more quickly than operations for conventional minerals.“

James Walker commented: “These recent processing advancements are tremendous to see. We have been continuously working at improving all our processes as we finish our mine planning and engineering work, and these metallurgy advances combine to greatly improve the economics of the project. These advances show much improved recoveries, meaning more product for market, as well possessing us with the knowledge and expertise to make an almost entirely pure product, several percent above the highest-grade purity required by industry. This advance gives us large margins of error that assure us a higher certainty of always meeting our manufacturing targets, while also preserving as much fluorspar as possible.”

Full size / Summary of Ares’ land position, volcanic breccia pipes and prioritized targets. Source

On January 11, 2021, Ares announced to have started preliminary planning for its second proposed mine site on its consolidated Spor Mountain property:

“The Company has identified the historic Bell Hill mine area as the most suitable site for an advanced mining operation, which is anticipated to operate concurrently with the Lost Sheep mine [LGP and Purple Pit}. The Bell Hill mine area exhibits several unmined fluorspar pipes identified by the USGS which appear at surface and appear to have continuity of fluorspar extending to depth. Exploration drilling will commence in the first quarter of 2021, which will inform an updated mine plan and outline the expanded operation. Sampling from the Bell Hill Claims has demonstrated high-grade fluorspar, further evidencing the uniformity of the high-grade fluorspar exhibited throughout the Spor Mountain range.“

“The Bell Hill mining area is the logical next area to be developed in the Spor Mountain Fluorspar District. The old mine works are located at the southernmost tip the range, at the lowest elevation, and most favourable topographic relief. The former past producing mines and prospects are still accessible by a network of well-maintained roads that will require minimal if any work for exploration and delineation purposes.“

James Walker commented: “We are very fortunate to have so many sites within our claims that offer the potential for further mining operations. The Bell Hill claims demonstrate several tightly located fluorspar pipes, offering an extensive source of feed for processing. Upon initiating operations on the Bell Hill claims the Company will seek to increase its processing and refining capacities to achieve greater outputs of its final fluorspar products.”

On November 12, 2020, Ares announced “the full completion of its fluorspar surveying work, identifying the most prospective mining areas across its 2,100 acre Spor Mountain operation areas“:

“Ares identifies over 30 mining prospects, for the purposes of short-term and long-term mine and operational planning, over the coming years... Work comprises major component of the Company’s mine plan, and one of the final pieces before planning is completed and construction can begin... The recent land acquisition resulted in the control of the majority of past producers, prospects, and newly identified targets.“

James Walker commented: “This is an important stage towards completing our mine plan and providing investors with a huge confidence of the potential and abundance of high-grade fluorspar in our area. Compiling this database of prospects also provides Ares with enormous insight into the scale of our project and the long-term operations we can expect from something this size. If these identified pipes are half the average volume of historic pipes, we would be operating for decades before exhausting only these mining prospects. These identified prospects will also be complimented by future exploration work to locate the rest of the fluorspar pipes which were severed by tectonic shifts from these identified targets. A special thank you to our geologist Raul Sanabria for all his hard work compiling all these prospects from data and geotechnical analysis.”

Full size / Flowsheet & Plant Design

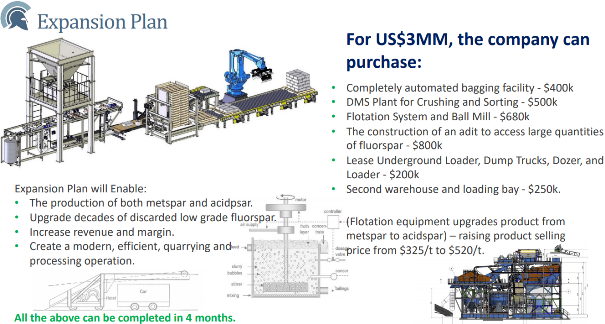

On December 22, 2020, Ares announced completion of “its engineering design work on the upcoming processing facility to be installed at the mining operation in 2021“:

“The Company has completed the full Process Design Criteria, and has assembled a proposal for equipment manufacturers, which includes flow-sheets. The full plant will take raw ore and produce an acidspar grade product, which is used in the manufacture of aluminum, refrigeration units, touch screens, fluorine, hydrofluoric acid, and electric car batteries. This high-end industrial product requires a fluorspar purity of 97%+, which the new plant will provide. Acidspar sells for a premium in the fluorspar market due to the vast number of industrial applications. The product composes over two-thirds of the United States’ fluorspar market, and is currently 100% imported from countries outside the United States.“

James Walker commented: “We hope to complete the tendering process and get started on the construction, delivery, and commissioning of the plant, immediately. This will be the largest acquisition ahead of the Company launching the US’ first completely domestic acidspar operation in decades. The Company is transitioning from its design and planning phase, into the construction and equipment acquisition phase of its mining operation. We are fortunate that all permitting is already in place, and only heavy machinery and a plant is required to commence mining. The plant is the longest lead item, so during its construction and installation, all construction can be completed, and all mining equipment can be purchased and installed. The Company is very pleased to be making good progress towards its mining goals, and anticipates a very successful 2021.”

On November 4, 2020, Ares announced “a US$10MM equipment leasing arrangement with Sertant Capital, LLC“:

“Ares intends to execute a 36-month leasing arrangement, during which [it] will purchase its flotation plant, heavy machinery and vehicles, crushing circuit, and bagging facility. The leasing arrangement will finance 90% of all equipment costs, with [Ares] being responsible for paying 10% of the leasing facility.“

James Walker commented: “This is a major development for the Company towards its mining operation and production plans. Getting the leasing arrangement in place will mean we can concentrate our efforts on completing the expanded mine plan and metallurgy, and then immediately begin equipment acquisitions. The mine is already fully permitted, so the delivery of the equipment to site will be the final stage before operations can commence. We have a 500 ton/day operation planned, and a demand which outstrips our supply. [Ares is] excited to be supplying North American industry with its the first domestically produced fluorspar in years, and to operate as the only permitted and producing fluorspar mine in the entire U.S.”

Full size / Source: Ares’ corporate presentation 2020

Bottom Line

Ares Strategic Mining Inc. appears to be making all the right moves at an impressive pace, professionally advancing the Lost Sheep Fluorspar project to the only fluorspar mine in the US and one of the world‘s highest grade fluorspar deposits.

Ares is backed by a strong management team experienced in engineering and mining.

Ares‘ CEO and President, James Walker, is a professional Mechanical and Mining Engineer experienced in project management, particularly within mining engineering, mechanical engineering, construction, manufacturing, engineering design, infrastructure, and safety management.

With over 20 years of experience, Ares‘ VP of Exploration, Raul Sanabria, worked for the Minersa Group, the largest European fluorspar producer with mines in Spain (capacity: 140,000 t annually) and South Africa (capacity: 240,000 t annually).

Importantly, Ares has already teamed up with strong technical and industrial partners as well as strategic investors.

In March 2020, Ares announced a strategic partnership with the Mujim Group, a large multinational fluorspar mining and distribution company (“highly profitable“) with mines in Thailand and Laos (capacity: around 100,000 t annually). With a 9% equity stake in Ares, the Mujim Group has agreed to invest time and expertise in assisting Ares‘ Lost Sheep mining and processing opration to achieve greater production levels and efficiency. The Mujim Group has committed to assist with equipment selection, mining methods, processing techniques, and the supply of expert fluorspar mining personnel, to ensure Ares’ mine achieves its potential.

Recently in late December, Ares announced to have received technology commitments from the Mujim Group, enabling Ares to produce a fluorspar product not previously anticipated at its Lost Sheep operation: Fluorspar lumps.

The Mujim Group “has developed a new technology able to produce fluorspar lumps from material that was previously unsuitable for their manufacture. The lumps product is ideal for use in ceramic, fiberglass, & glass industries, and reduces the refractory melting point, promotes the flow of slag, and enables the separation of slag and metal. This product also assists with desulfurization and dephosphorization during the smelting process, and acts to enhance the tensile strength of forged metals, making it extremely valuable and important to metals manufacturers... Due to the industrial applications and relative rarity of fluorspar lumps, the product often commands higher retail prices than more refined and pure fluorspar products, potentially offering Ares a new and improved income stream. Currently the United States imports 100% of this product for its industrial base, so the Company has the potential to be the first vertically integrated lumps manufacturer in the country. This manufacturing line would run alongside Ares’ already anticipated plant and manufacturing facilities, and will afford it a broader range of industrial products.“

In the mining business, normally a lot of exploration and development work must be completed before a mining decision can be made.

With Ares having closed the Lost Sheep project acquisition in late February 2020, and starting to trade on the TSX-V in early March, today‘s announcement is enabling the company to now complete its mine planning as the final drill results can now be fitted to a block model, and the optimum mining methods can now be finalized. As soon as Ares completes its Mine Plan, construction of the mine and processing facility can start.

Upgrading mined fluorspar material does not require a chemically intensive processing plant with a complicated and capital-intensive flowsheet components as being the case with some gold mines for example. At Lost Sheep, only drilling to the bottom of the pipe is needed, followed by a drill and blast mining operation with conveyor belts transporting material to a dump truck bringing it into a crusher and then into floation to produce acidspar. Some of the material might be of such high grade that it could be sold as DSO (Direct Shipping Ore) for metspar users. The waste is so clean that it can be put back into the mined out pits. Ramping up the operation is relatively simple.

What makes Lost Sheep so special is its naturally occuring high grades of fluorspar with low impurities (basically no sulfides, no oxides, no arsenic). Competing mainly with Mexican fluorspar high in aresenic (heavily penalized), Ares is on a mission to become one of the major suppliers to the US market with a current demand of an estimated 600,000 t fluorspar annually (“normal levels“: well above 1 million t).

Full size / Source: Ares’ corporate presentation 2020 / Disclosure: Companies typically rely on comprehensive feasibility reports on mineral reserve estimates to reduce the risks and uncertainties associated with a production decision. Some industrial mineral ventures are relatively simple operations with low levels of investment and risk, where the operating entity has determined that a formal prefeasibility or feasibility study in conformance with NI 43-101 and 43-101 CP is not required for a production decision. The Company has not completed a feasibility study on, nor has the Company completed a mineral reserve or resource estimate at the Lost Sheep Mine and as such the financial and technical viability of the project is at higher risk than if this work had been completed. Based on historical engineering work, geological reports, historical production data and current engineering work completed or in the process by Ares, the Company intends to move forward with the development of this asset. The Company further cautions that it is not basing any production decision on a feasibility study of mineral reserves demonstrating economic and technical viability, and therefore there is a much greater risk of failure associated with its production decision. In addition, readers are cautioned that inferred mineral resources are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves. The development of a mining operation typically involves large capital expenditures and a high degree of risk and uncertainty. To reduce this risk and uncertainty, the issuer typically makes its production decision based on a comprehensive feasibility study of established mineral reserves. The Company has decided to proceed without established mineral reserves, basing decision on past production and internal projections.

Once the plant is up and running, positive cash-flows could be used to develop its other project: The Liard Fluorite property, “the most significant fluorite prospect in British Columbia“. James Walked commented: “This is a major step towards fulfilling our ambition to operate multi-nationally. We own the only permitted fluorspar mine in the USA, which we are currently developing for greater production, and once operational we will begin development work on our Canadian project. With this acquisition, Ares is mitigating against global uncertainties by diversifying its portfolio and its countries of operation. Fluorspar is an industrial mineral the world is struggling to adequately acquire, and we are positioning ourselves well to supply that need.”

If the Western world was to be cut off from fluorspar supply, or running out of it, many industries would come to a standstill or face major difficulties:

• The production of aluminium and steel requires fluorspar in form of acidspar and metspar, respectively, which are used as a flux to lower the temperature of the slag and to increase its reactivity for removal of impurities.

• Steel mills require 4.5-9 kg (10-20 lb) of fluorspar per ton of steel (or about 3 kg / 6.5 lb of metspar).

• Aluminium producers require about 27 kg (60 lb) of high-grade fluorspar per ton of aluminium (“fluoride consumption... averages 60 lb of aluminum fluoride and 50 lb of synthetic cryolite [produced by reacting diluted hydrofluoric acid and aluminium hydrate] per ton of aluminum ingot produced. This is equivalent to about 70 lb of HF [hydrofluoric acid] per ton of aluminum. In the United States, the amount of HF required is probably 20% less, or 56 lb/ton, owing to recycling of fluoride values from spent potlinings and flue gases, as well as the manufacture of aluminum fluoride and synthetic cryolite from fluorosilicic acid.” McKetta, Encyclopedia of Chemical Processing and Design).

• Roskill estimates that half of all new medicines contain fluorspar derivatives.

• Exploration for metals relies on drilling, whereas the analysis of drill core samples sometimes relies on hydrofluoric acid (produced from acidspar) due to its ability to efficiently dissolve most oxides and silicates.

• The mining industry oftentimes requires hydrofluoric acid for separating ore from surrounding material.

It would be bold to call fluorspar the world‘s most important commodity, but what other mineral or element could possibly be a contender?

Source: https://youtu.be/J5vWLF0AKmE

In Greek myths, Ares embodies the physical valor necessary for success in war. (Image)

Background

Ares is the Greek god of war. Indeed, there is a kind of war happening around the globe, a fight for fluorspar supply.

And just like Ares playing a relatively limited role in literary narratives of Greek mythology, you don‘t hear much about fluorspar in the media, on the internet or from newsletter writers. Why? I bet it‘s because there are so very few publicly listed companies focussed on fluorspar. Most fluorspar miners are from China, are privately held companies, or belong to large chemical and industrial conglomerates with multi-billion-dollar market capitalizations.

As a consequence, many investors underestimate how dangerously critical fluorspar has become for global economies and how exceedingly rare it is to find a primary fluorspar miner listed on a stock exchange in the Western world.

However, once having realized fluorspar‘s strategic economic importance in today‘s world, it‘s difficult not to fall in love with a fluorspar company like Ares Strategic Mining – just like Aphrodite, the Greek goddess of love, losing her heart to Ares and, as a consequence, giving birth to Eros, the Greek god of love.

In a similar fashion, Ares Strategic Mining and its other half (investors, industry partners and backers) are on a mission to give birth to a new, domestic fluorspar mining and beneficiation industry in the US as the nation has been 100% import-reliant on fluorspar since 1997 and is eager to break free from its foreign dependency on fluorspar supply.

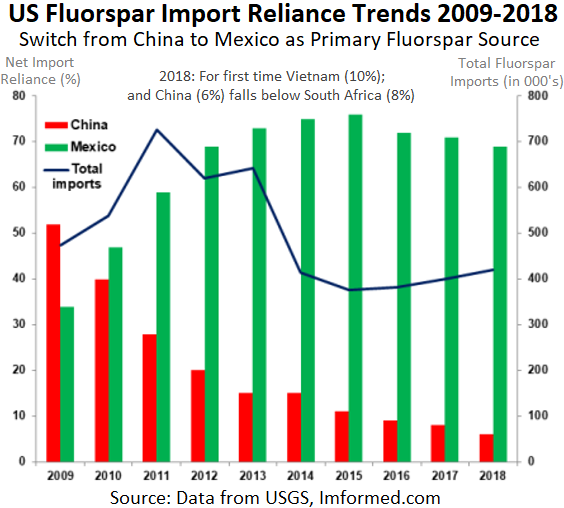

The US has evolved from China-reliant to Mexico-reliant for fluorspar imports, however most Mexican fluorspar comes from a single Mine (Las Cuevas).

Fluorite (called “fluorspar“ in the industry) is one of the most abundant minerals on this planet, widely dispersed in the earth‘s crust. However, it‘s all the more rare to find high enough grades (>20% CaF2) and quantities to justify a primary fluorspar mine. As such, fluorspar is produced mostly as a by-product from mining other commodities, first and foremost rare earth elements (above all China) and silver (above all Mexico).

With Mexico being by far the most important fluorspar supplier to the US, recent supply disruptions revealed the urgent need to diversify supply chains. More and more companies are waking up and realizing how dangerous it is to rely on a single supplier, or country, for their raw materials.

Recently, the Las Cuevas Mine in Mexico was at risk of closure due to COVID-19 safety restrictions imposed by the government. This prompted companies like GlaxoSmithKline and Cipla, two of the world‘s largest manufacturers of inhalers used by patients with respiratory diseases (the group most vulnerable to COVID-19), to send letters of urgency to Las Cuevas‘ owner (Orbia Advance Corp.; market cap: $3.6 billion USD) and the Mexican government to keep the mine in operation. About 80% of the world‘s inhalers use fluorspar which is mined at Las Cuelvas, the largest fluorspar producer in the world accounting for around 20% of global supply. “Without the mineral [fluorite], the medical supply chain is dead,“ said Sameer Bharadwaj, President of Koura, Orbia‘s fluorspar branch, and added: “Many of our customers are out of supply and we are receiving more orders because they are anticipating increased demand for COVID-19.“

Mexico, Vietnam, South Africa, and China currently supply more than 90% of US fluorspar demand. With a share of about 70%, Mexico accounts for the single most important source of fluorspar imports into the US. However, Mexico‘s largest fluorspar producer, Orbia, has an evolving strategy to use more of its own fluorspar for downstream value-added speciality fluor products (e.g. hydrofluoric acid, refrigerant gases, aluminium fluoride) with fewer fluorspar exports available for US companies such as Honeywell and Chemours (DuPont‘s spin-off in 2015). As Orbia becomes more vertically integrated, there is a danger for its US customers that more and more fluorspar becomes unavailable (2015: 60% of Orbia‘s fluorspar was sold to the open market, including the US).

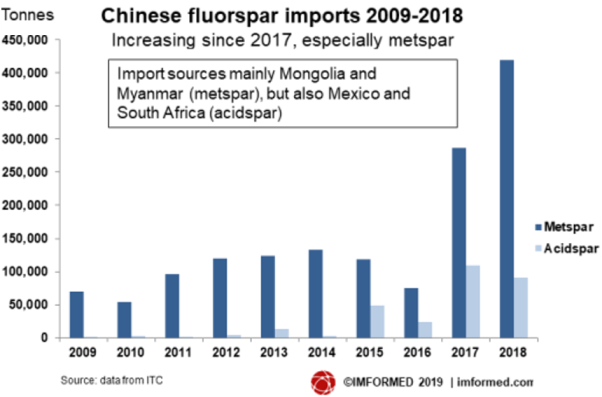

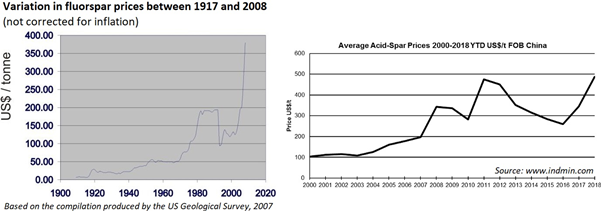

With China accounting for around 60% of global fluorspar mine supply, there is not much margin of maneuver for US companies requiring fluorspar to keep their businesses alive, especially when considering that China has become a net importer of fluorspar in 2017, a major shift that sent market prices skyrocketing and reaching multi-year highs in 2018 and 2019. The shock wave continues to be felt in the market as China used to be the number one exporter of fluorspar to the Western world.

With COVID-19 disrupting global trade and supply chains, domestic supply of critically needed commodities, especially fluorspar, is urgently needed in the US. Many governments (including the US, EU, and China) have classified fluorspar as a critical or strategic mineral as it can not be recycled and is vital for a number of large and important industries, putting economies and health systems at risk. The US is the 4th largest producer of crude steel and the world‘s largest manufacturer of hydrofluoric acid (Honeywell and Chemours). Both industries rely heavily on fluorspar. An estimated half of all new medicines contain fluorspar derivatives. According to Executive Orders 13817 (December 2017) and 13953 (September 2020), US producers of “critical minerals“ can expect government support, such as expedited permitting, federal investments in mining and processing, tax incentives, and data sharing.

Full size / Metspar: 60-85% CaF2 / Acidspar: ≥97% CaF2

Fluorspar Growth Drivers

According to Verified Market Research (August 2020):

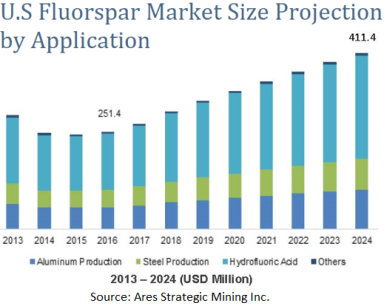

“Fluorspar Market was valued at USD 2.6 Billion in 2019 and is projected to reach USD 6.1 Billion by 2027, growing at a CAGR of 4.8% from 2020 to 2027.”

According to Global Market Insights (December 2020):

“Global fluorspar market share is depicting immense traction majorly due to extensive application of the compound in the manufacturing of steel and aluminum. Increasing disposable income among people along with urbanization has driven the need for construction of residential and non-residential buildings, primarily in developing nations like Asia Pacific and Latin America. Additionally, increasing use of fluorochemicals in various critical industries will positively influence the product demand.

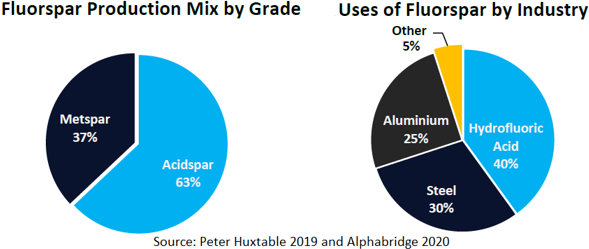

“The fluorspar market segments based on product are classified as metspar, acidspar, ceramic, and others. As per volume, acidspar, that is primarily converted into hydrofluoric acid with the help of sulfuric acid, holds the highest segmental share. In the manufacturing of synthetic cryolites and organofluorides, hydrofluoric acid is extensively used. These factors and staggering revenue will boost the fluorspar industry share from acidspar is expected to grow at 8% CAGR through 2024.

“In terms of application, fluorspar industry is classified into four main segments namely, steel production, aluminum production, hydrofluoric acid, and others. Hydrofluoric acid is one of the strongest inorganic acid that is extensively used for industrial purposes. With respect to revenues, hydrofluoric acid segment is projected to witness a CAGR of over 8% during the period of study.“

“Proliferating demand for ceramic parts in several industries like engineering, biomedical, electronics, chemicals, and aerospace is a primary factor supporting the demand for the product. They carry superior thermal stability at high temperatures and find usage in high-temperature environments. These products are porous, hard and brittle in nature and as a result, are also used to make bricks, pottery, cement, tiles and glass. The ceramic segment is subjected to record nearly 7.5% CAGR up to 2024.“

According to Transparency Market Research:

“The growth of the global [fluorspar] market is primarily driven by increasing demand for fluorochemicals. Moreover, the growth is also driven by the increasing requirement of steel and aluminum due to the flourishing construction sector. The growth of the market is also influenced by the growing use of fluorspar in the lithium ion batteries.

“The companies in the [fluorspar] market are pouring heavy resources in order to establish themselves above their competitive rivals. Moreover, it is projected that new players will enter the global market in the near future. This is projected to intensify the competition among the players and help driving the overall market development. The companies in the global market are expected to resort to aggressive growth strategies such as mergers, acquisitions, takeovers, strategic alliances, and partnerships in order to stay ahead of the competitive curve. These players in the market are expected to leverage the state of the art technologies and constant technological advancements to their benefit and generate more profits and expand their business.

“Acidspar Emerges as In-demand Product Segment: [The acidspar] segment [...] is expected to remain a highly profitable product segment... Acidspar is primarily employed in the production of hydrofluoric acid, which is further employed in the manufacture of fluorocarbons such as hydrofluorocarbons (HFC) and hydrochlorofluorocarbons (HCFC). In addition to that, fluorspar is utilized to produce fluoropolymers and cryolite. Cryolite is mostly used in aluminum smelting. Furthermore, aluminum fluoride (AlF3), which is employed in aluminum smelting, is mostly derived from acidspar. It is also employed to produce sodium fluoride salts, which are used in toothpastes. In terms of value and volume, acidspar was followed by metspar...

“Metspar is utilized as flux in the production of steel, as it helps lower the melting point of the metal. This saves money and energy. Metspar is employed in the metal manufacturing process to remove impurities such as sulfur and phosphorus. Ceramic grade fluorspar has applications in the production of ceramics, specialty ware, and enamel ware. Others segment, such as optical grade and lapidary grade, held minimal share of the global fluorspar market...

“Application-wise, hydrofluoric acid contributed to 40% share of the demand in the global fluorspar market. However, increasing investments in infrastructure projects globally is augmenting the demand from aluminum and steel production application.“

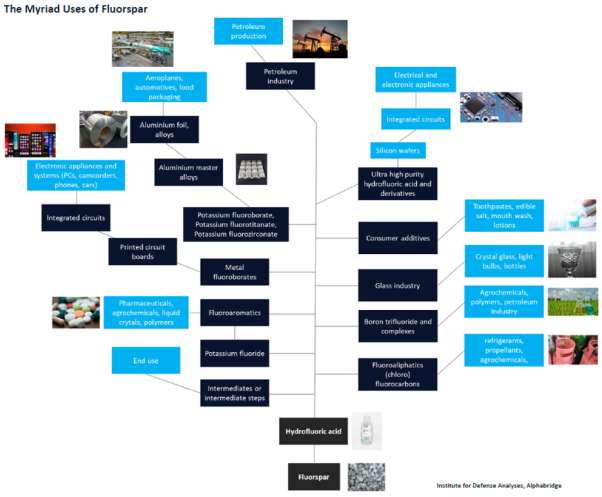

Full size / Fluorspar is a valuable commodity with a global market value of $2.6 billion USD in 2019. However, fluorspar‘s true value lies in the multiple downstream levels and applications (where it is oftentimes used as an indispensable component) worth approximately $120 billion USD annually. Downstream applications and end uses include (amongst others) lithium batteries, composites for automobiles, aerospace applications, microelectronic sensors, solar panels, LCD screens, speciality coatings (e.g. Tefal, Gore-Tex, flame retardant clothing), ceramics, glass, food packaging, active pharmaceutical ingredients, anaesthetics, toothpaste, mouth wash, agrochemicals, light bulbs, refrigerants, nuclear power. Major consumers of acidspar and hydrofluoric acid include Orbia (ex-Mexichem), Honeywell, Chemours (ex-DuPont), Daikin, Solvay, Lanxess, Fluorsid, DDFluor.

Fluorspar Mining

For many key industries, there exist no substitutes for fluorspar. As fluorspar is consumed by the industry, it cannot be recycled and thus must be mined on a continuous basis.

The US used to be the world‘s number one fluorspar supplier (1910-1950s). Due to foreign competition, its dominance shrank thereafter, with only one fluorspar producer left in 1982. By 1997, the entire US fluorspar mining industry was wiped out. Since then, the US has been a 100% net importer of fluorspar.

“Depleting high quality fluorspar reserves, high cost of acidspar production, and likely continued pressure and perhaps further capacity reductions in China, combined with continuing demand for fluorspar in chemical, steel and aluminium markets mean that there is a case for alternative and new fluorspar sources to come on line.“ (Imformed Industrial Mineral Forums & Research, 2019)

Fluorine‘s (F) abundance in the solar system is exceptionally low. Yet in the earth‘s crust, it‘s one of the more abundant elements and is widely dispersed in nature. Elemental fluorine does not occur naturally. Instead, all fluorine exists as fluoride-containing minerals. Many fluorine-bearing minerals are known, but of paramount commercial importance is fluorite (CaF2). There exist only few primary fluorspar mines in operation globally today. Fluorite is not an uncommon mineral and can be found on all continents, but it is exceptionally rare to find high enough grades (>20% CaF2) with large enough quantities to justify a commercial mine.

Mined fluorite does not require sophisticated hydrometallurgical processing and only requires physical upgrading to a high enough purity for the target end-use. Most fluorspar ores require upgrading through beneficiation suited to the source and end markets. Metspar is produced by sorting, crushing, grinding and sieving, while acidspar also requires removal of impurities by flotation. High metspar grades with small grain size are favored by steel mills (faster reactivity times) and have been selling for a premium in the past.

St. Lawrence Fluorspar Mine

Location: Newfoundland, Canada

Operator: Canada Fluorspar Inc. (private)

Resources: 9.1 million t @ 42% CaF2 (Indicated) and 1 million t @ 31.1% CaF2 (Inferred)

Life of Mine: 30 years

Capacity: 200,000 t acidspar annually (after ramp-up and mill commissioning)

Pre-Production CAPEX: $154 million

Deposit: Fluorite veins

Mine: Open-Pit (underground thereafter)

Operation Start: 1930s-1978, 2017 (first shipment of 5,000 t acidspar to the US in 2018)

Notes: In 2011, Arkema Inc. (current market cap: 7 billion EUR) invested $15.5 million for a 19.9% equity stake in Canada Fluorspar. Thereafter, both formed a 50/50 partnership funded by Arkema ($60 million) and Canada Fluorspar ($14 million). In 2014, Canada Fluorspar was acquired by US-based private equity firm Golden Gate Capital in an all-cash deal at of $0.35/share (~66% premium to prior trading range). This valued the deal at $39 million, based on 111 million shares at that time. The stock was delisted shortly thereafter. If fluorspar was better known to investors back then, the sales price might have been higher considering the magnitude of the mine‘s projections (200,000 t acid-spar x $500/t = $100 million annually x 30 years = $3 billion).

(Source #1; Source #2; Source #3)

Nokeng Fluorspar Mine

Location: South Africa

Operator: SepFluor Ltd. (private)

Reserves: 3.2 million t CaF2 (12 million t @ 26.6% CaF2)

Life of Mine: 19 years

Capacity: 180,000 t acidspar and 30,000 t metspar annually (with plans to add value by also producing hydrofluoric acid and aluminium fluoride)

Pre-Production CAPEX: $140 million

Deposit: Hematite-Fluorite

Mine: Open-Pit

Construction Start: June 2017

Operation Start: August 2019 (maiden shipment of 10,000 t acidspar to the US in December 2019)

Notes: Unique flotation process developed due to high iron content. One of only three significant fluorspar production newcomers in the past 10 years. South Africa‘s second active fluorspar mine. SepFluor has agreed to sell the 40% forward fixed at prices between $240-260 per t in exchange for funding (Debt: Consortium of Nedbank along with Dutch and German development banks; Equity: Led by David Twist, Rudolph de Bruin, Carlo Baravalle).

(Source #1; Source #2; Source #3)

Vergenoeg Fluorspar Mine

Location: South Africa

Operator: MINERSA Group (private)

Reserves: 174 million t @ 28.1% CaF2

Life of Mine: >100 years

Capacity: 240,000 t acidspar and metspar annually

Deposit: Hematite-REE-Fluorite

Mine: Open-Pit

Operation Start: 1956

(Source)

Doornhoek Fluorspar Project

Location: South Africa

Operator: Eurasian Resources Group (private)

Resources: 516 million t @ 13.82% CaF2 (Indicated + Inferred)

Life of Mine: >100 years

Capacity: 240,000 t acidspar annually

Deposit: Dolomite-Quartz-Pyrite

(Source #1; Source #2)

Ashram REE-Fluorspar Project

Location: Quebec, Canada

Operator: Commerce Resources Corp. (listed on TSX.V: CCE)

Resources: 28 million t @ 5.9% CaF2 and 1.9% REO (Indicated) and 220 million t @ 4.5% CaF2 and 1.88% REO (Inferred)

Capacity: 70,000 t metspar annually potentially (at 75% recovery) as a REE by-product

Deposit: Carbonatite-REE-Fluorite

Notes: One of the world‘s largest REE and fluorspar resources (at pre-feasibility stage).

(Source #1; Source #2)

Niobium Claim Group Project

Location: Quebec, Canada

Operator: Saville Resources Corp. (listed on TSX.V: SRE) optioned the project from Commerce Resources Corp.

Deposit: Carbonatite-Niobium-Tantalum-Phosphate-Fluorite

Notes: Adjacent to the Ashram Project. Drill intercepts such as 235.35 m of 9.8% CaF2 and 1.92% TREO (hole EC15-133) showed high grades of middle and heavy rare earth oxides along with appreciable fluorite grades occurring near surface over the entire hole (from 3.65 m to 239 m). Fluorspar is a potential by-product.

Management & Directors

James Walker (President, CEO, Director)

Mr. Walker has extensive experience in engineering and project management, particularly within mining engineering, mechanical engineering, construction, manufacturing, engineering design, infrastructure, safety management, and nuclear engineering. His professional experience includes designing nuclear reactors, submarines, chemical plants, factories, mine processing facilities, infrastructure, automotive machinery, and testing rigs. Mr. Walker holds degrees in Mechanical Engineering, Mining Engineering, and Nuclear Engineering, as well as qualifications in Project Management and Accountancy, and is a Chartered Engineer with the IMechE, registered as a Project Manager Professional with the APM, and registered with APEGA as an Engineer.

Raul Sanabria (VP of Exploration, Fluorspar Expert, Director)

Mr. Sanabria has over 20 years of international experience as an exploration and mine geologist in a variety of mineral deposits. He started his career working 5 years for Minersa Group, the largest European fluorspar producer. He recently worked as Senior Exploration Manager for Tudor Gold Corp., VP Exploration for Rover Metals Corp., Chief Geologist for Red Eagle Exploration Ltd., and VP of Exploration at American Creek Resources Ltd., G4G Resources Ltd., and Northern Iron Corp. He was President and CEO at Condor Precious Metals Inc. Currently, he is President at Malabar Gold Corp./Minera La Fortuna SAS focused on small-scale gold production and toll milling in Colombia.

Michael Changxian Li (Director)

Mr. Changxian Li has 29 years of experience in trading and investing in iron ore and steel-related raw materials and finished steel products. In the 1990s, Mr. Li devoted himself to bulk commodity trade of iron ore, steel scrap, coal, ferro-alloy, base metals, and non-metallic minerals. Since 2008, Mr. Li also started mining investments in Australia, the US, and Canada. Previously, he worked 13 years at Mitsubishi Corp. and its metals division, where he, as a senior manager, was responsible for trading operations among China, Japan, India, South Korea, the US, Canada, Australia, and Chile. In July 2004, Mr. Li became independent and established his own company based in Hong Kong to continue international trade of steel-related raw materials and finished steel products. Mr. Li is the Co-Founder and CEO of OMC Investment Co. Ltd. in Hong Kong, and also the Co-Founder and CEO of Vantage Asia Holdings.

Karl Marek (Director)

Mr. Marek has been involved in the public markets for over 20 years, during which time he served in due diligence, deal sourcing, marketing, and capital raising. He began his career in sales at a Vancouver investor relations company, and in 2007 he started his own multi-tiered marketing firm which quickly rose to become an industry leader in their field. Within 2 years, the said company was a buyout target for one of the world’s most influential marketing companies and was sold. For the past 8 years, Mr. Marek has started and been running a successful private boutique equity firm that has consistently shown large annual returns. He has the been involved in projects ranging from technology to bio fuel, clean coal, oil and gas, and mining exploration.

Paul Sarjeant (Director)

Mr. Sarjeant is a professional geologist with mineral exploration and development experience in North and South America and throughout Africa, Asia, and Europe. His career in mineral exploration spans 25 years. He has extensive experience having served as President and CEO roles for several small-cap exploration and development companies and is currently a Director and Consultant to a number of private and public mining companies. He is also the President, CEO and Founder of Doublewood Consulting Inc. providing technical and management services to the mineral exploration industry. He holds a BSc (honors) degree in Geological Sciences from Queen‘s University in Kingston (Ontario) and is a Member of the Association of Professional Geoscientists of Ontario. Mr. Sarjeant is the Qualified Person for Northern Iron Corp. under NI 43-101.

Bob Li (Director)

Mr. Li is the Chairman and Managing Director of the Mujim Group, one of Asia‘s largest fluorspar producers. He operates several fluorspar mines in Thailand and Laos, as well as fluorspar trading companies in India, China, and the UAE. He also serves as the Board Chairman of Yixin Mining, Bright Biz Mining, Bun Nun Mining, Dihao Investment Co, Everbright Fluorchemicals, L&S International Trading, and Green Efficiency Mining. He has worked as a Representative at Gujarat Fluorochemicals and as the Deputy General Manager at Hengyuan Tech Chemical Co, and is a Board Director at Delong. He brings to Ares many years of operational experience in the fluorspar industry, as well as his expertise, and knowledge of fluorspar equipment and processing. When Mr. Li was appointed in June 2020, James Walker commented: “It’s a major coup to bring in someone as experienced with fluorspar mining and processing as Mr. Li. After visiting his mines in Thailand and seeing the scale, organization, and technology of his operation, we cannot imagine a better partner and Director to ensure the Company successfully achieves a profitable and efficient mining operation. This development hugely assists to de-risk our project as we will benefit from years of honed fluorspar mining practices. We look forward to working with Mr. Li in the coming months as we advance towards mining and production.”

Viktoriya Griffin (CFO)

Mrs. Griffin is a dedicated and knowledgeable Chartered Accountant who has over a decade of experience in the field. She started her career by leading audit and assurance services for public companies and large international accounting firms, including Deloitte in the UK and Ernst & Young in Canada. Most recently, she led the CFO services line at Clearline CPA. She is now the CFO for a number of public companies on TSX Venture Exchange with national and international operations. She provides financial insights and strategic advice enabling businesses to grow. She is also an active supporter of her community by being a Board Member and the Chair of the Audit & Finance Committee of Habitat for Humanity of Greater Vancouver.

Tom Klaimanee (Corporate Secretary)

Mr. Klaimanee has a wealth of international and management experience. He provides administrative services to private and publicly listed companies. He holds a Master of Business Administration degree from the University of Southern Mississippi, USA.

Dace Church (Creative Arts and Media Manager)

Mrs. Church has 8 years of experience working in the precious and base metals industry. She holds a Bachelor‘s degree in Marketing. In addition to her commitments at Ares, Mrs. Church is an Executive Assistant of Otso Gold Corp.

Ares appoints Keith Minty to oversee its fluorspar mine construction and commissioning

In August 2020, Ares appointed Keith Minty (P. Eng., MBA) to the position of Vice President - Project Manager, responsible for coordinating, progressing, and launching, commissioning Ares’ new expanded fluorspar mining operation in Utah. He has extensive experience leading the construction and commissioning of 9 mines worldwide, including the largest open-pit palladium operation in North America. He has been employed as Senior Mining Engineer, Mine Superintendent, Mine Designer, and CEO and President. Mr. Minty obtained a B.Sc. in Mining Engineering from Queen’s University, Kingston Ontario in 1978 and an MBA from Athabasca University in 2014. He has over 30 years of international and domestic mine development and operating experience as a successful mine builder, developing dozens of projects from exploration stages through to production on several different continents. Mr. Minty is a past Northern Miner’s “Mining Man of the Year” recipient. Among Mr. Minty’s previous projects, he restructured the only North American platinum group metal project with a $350 million CAD initial public offering and developed North American Palladium Ltd. as the world’s 5th largest platinum group metal producer, with the lowest operating cost and the highest productivity. In October 2019, South Africa‘s Impala Platinum Holdings Ltd. (current market cap: $11 billion USD) bought Canada-based North American Palladium Ltd. for about $1 billion CAD. James Walker, President and CEO of Ares, commented: “We’re extremely pleased to welcome someone of Mr. Minty’s experience to our Company. His project development experience will be an invaluable asset to the company during the development stages of our Lost Sheep Mine. Having Mr. Minty’s assistance, and project development experience at our operation will greatly benefit Ares. We consider his involvement to be a major validation of our plans and future ambitions. We are very pleased to welcome him into the Company and are excited for the upcoming project development work, and to take advantage of his extensive professional experience.” After examining the Lost Sheep Mine and its potential, Mr. Minty has agreed to settle 60% of his future Invoices in Company Stock through a Shares for Debt Settlement. Mr. Minty has already commenced work on the Lost Sheep mine, bringing his experienced team and contacts to advance the mine to production.

Ares appoints Process Engineer and Metallurgist Denise Nunes

In March 2020, Ares appointed Denise Nunes, a process engineer and metallurgist with over 20 years of experience, including employment with Ausenco, SRK Consulting, SGS, and JDS Energy & Mining. She has been employed to oversee the metallurgical and bench testing for Ares, and based on the results, design a processing facility for the Lost Sheep Mine to produce acidspar and high-grade metspar for industry. James Walker commented: “We are very pleased to have someone of Denise’s caliber join the team. Already Denise’s initial work is proving extremely promising for our future operations. We believe that with Denise’s expertise and professionalism we can design, build, and install the facility necessary to achieve the best capacity and quality for the Company’s ambitions.”

Videos: Presentations & Interviews

Click above image or here to watch (January 22, 2021)

Click above image or here to watch (January 22, 2021)

Click above image or here to watch (January 7, 2021)

Click above image or here to watch (November 12, 2020)

Click above image or here to watch (November 7, 2020)

Click above or here to watch (October 28, 2020)

Click above or here to watch (October 2, 2020)

Click above or here to watch (September 14, 2020)

Company Details

Ares Strategic Mining Inc.

Suite 1001 – 409 Granville Street

Vancouver, BC, V6C 1T2 Canada

Phone: +1 604 345 1576

Email: info@aresmining.com

www.aresmining.com

ISIN: CA21871U1057

Shares Issued & Outstanding: 88,203,221

Canadian Symbol (TSX.V): ARS

Current Price: $0.60 CAD (01/26/2021)

Market Capitalization: $53 Million CAD

German Symbol / WKN: N8I1 / A2PZ3F

Current Price: €0.404 (01/26/2021)

Market Capitalization: €36 Million EUR

Contact:

Rockstone Research

Stephan Bogner (Dipl. Kfm.)

8260 Stein am Rhein, Switzerland

Phone: +41-44-5862323

Email: info@rockstone-research.com

www.rockstone-research.com

Disclaimer: This report contains forward-looking information or forward-looking statements (collectively "forward-looking information") within the meaning of applicable securities laws. Forward-looking information is typically identified by words such as: "believe", "expect", "anticipate", "intend", "estimate", "potentially" and similar expressions, or are those, which, by their nature, refer to future events. Rockstone Research, Ares Strategic Mining Inc. and Zimtu Capital Corp. caution investors that any forward-looking information provided herein is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to the Ares Strategic Mining Inc.´s public filings for a more complete discussion of such risk factors and their potential effects which may be accessed through their profiles on SEDAR at www.sedar.com. Please read the full disclaimer within the full research report as a PDF (here) as fundamental risks and conflicts of interest exist. Ares Strategic Mining Inc. pays Zimtu Capital Corp. to provide this report and other investor awareness services.The author, Stephan Bogner, holds a long position in Ares Strategic Mining Inc., Commerce Resources Corp., Saville Resources Inc., and Zimtu Capital Corp., and is being paid by Zimtu Capital Corp. for the preparation and distribution of this report, whereas Zimtu Capital Corp. also holds a long position in all of the featured companies, Ares Strategic Mining Inc., Commerce Resources Corp., and Saville Resources Inc.