Over the past 2 years, precious metals have quietly transitioned from consolidation into full bull market mode.

Gold has already pushed into uncharted territory, breaking decisively above its 2011 high, while silver has staged an equally powerful comeback and is now testing key levels not seen in over a decade.

This shift is no coincidence. Mounting macro pressures – from record sovereign debt and persistent inflation to escalating geopolitical risk – are driving renewed demand for monetary metals.

At the same time, structural forces such as electrification and the recognition of silver as a U.S. “critical mineral” are reinforcing the case for silver as both a strategic resource and an investment vehicle.

Against this backdrop, both gold and silver charts point higher, with technical setups aligning with strong fundamentals to suggest that the precious metals bull market is still in its early stages.

Full size / Gold since September 2023: The chart shows a clear sequence of consolidation phases (white triangles) followed by decisive breakouts (green circles). Each breakout has driven prices to new levels within the long-term ascending channel. The most recent breakout above $3,400 suggests continuation of the trend, with momentum firmly intact.

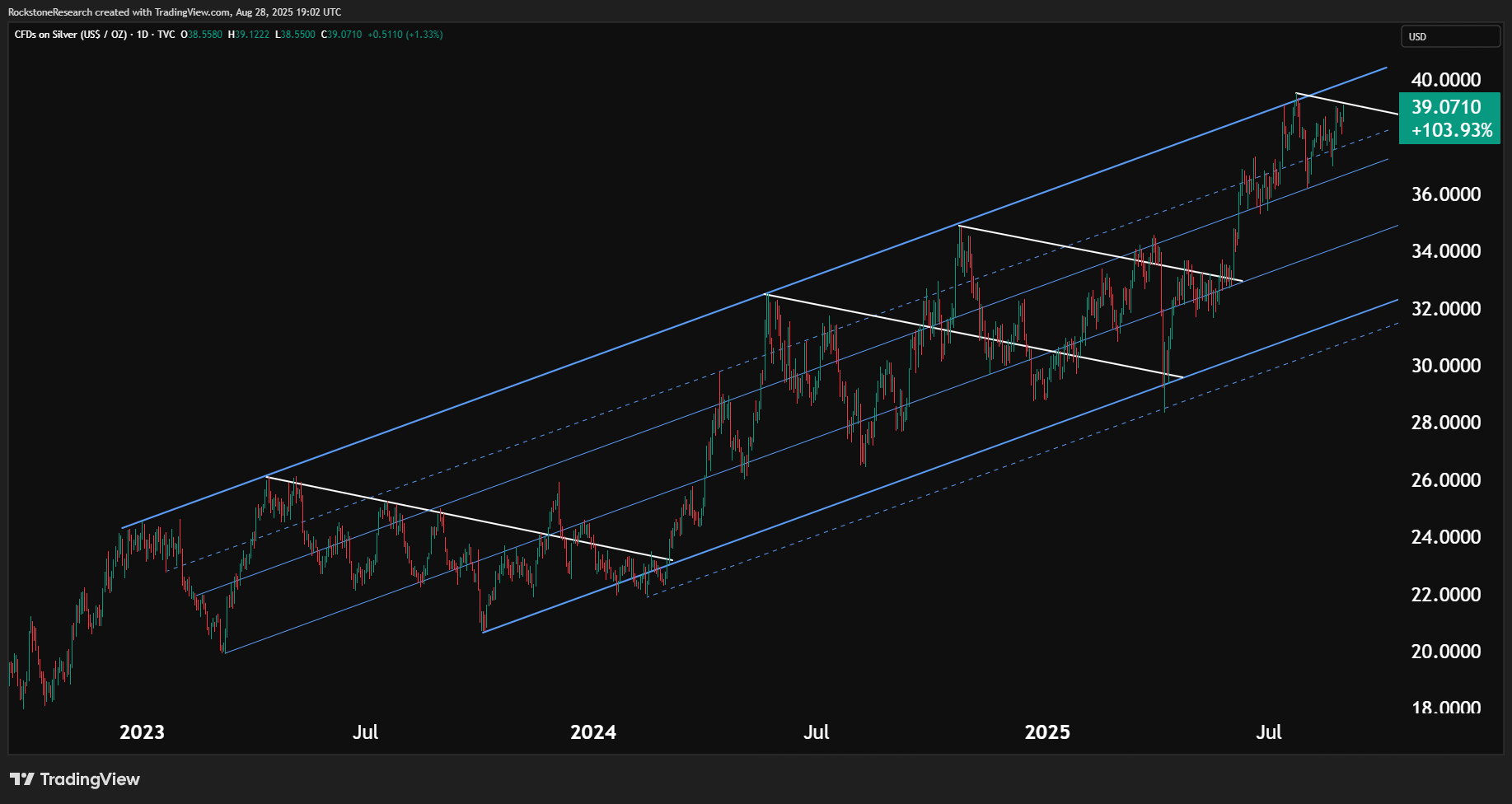

Full size / Silver since September 2022: The price action mirrors gold’s earlier move, with repeated consolidations resolving upward. Currently trading at $39/oz, silver is looking to break above the $40 level now. Despite strong gains in the last few years, silver remains well below its 2011 peak near $50/oz, while gold has already surpassed its 2011 high by a wide margin.

Fundamental Drivers for Gold

Several macroeconomic and geopolitical factors continue to underpin gold’s rally:

• Debt and Deficits: Rising global debt levels, particularly in the U.S., are eroding confidence in fiat currencies.

• Geopolitical Risk: Escalating conflicts and trade tensions are reinforcing gold’s role as a safe-haven asset.

• Real Interest Rates: Despite higher nominal rates, persistent inflation keeps real yields low or negative, favoring gold.

• Central Bank Purchases: Sovereign demand for gold remains at record levels as countries diversify reserves away from the U.S. dollar.

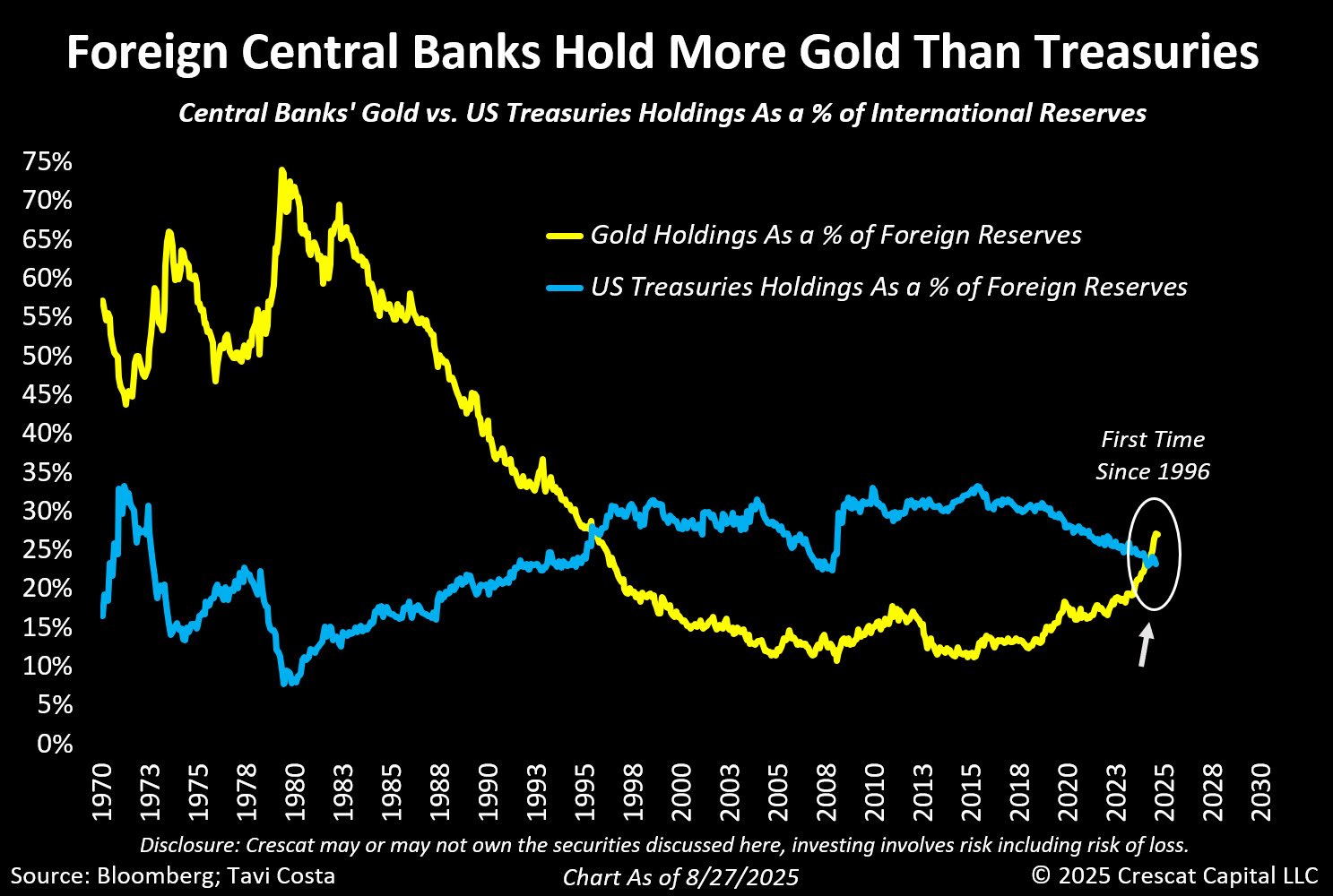

Central Banks as Drivers of Gold Demand

Full size / "Foreign central banks now officially hold more gold than US Treasuries — for the first time since 1996. Let that sink in. If you think this buying streak is ending, just look at what happened in the 1970s. This is likely the beginning of one of the most significant global rebalancings we´ve experienced in recent history, in my view." (Tavi Costa)

• This shift marks a historic turning point: For decades, gold had steadily lost ground to U.S. Treasuries – but now the balance has reversed.

• For investors, it underscores that gold demand is no longer driven solely by private buyers, but increasingly by sovereign actors. This structural reallocation of global reserves is providing powerful tailwinds for the ongoing gold bull market.

Silver: Strengthening the Investment Case

Contact:

Disclaimer: This article is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell commodities. The author holds physical gold and silver, stored in Central Switzerland through Elementum International AG. The author does not hold any direct interests or financial instruments related to other commodities or companies mentioned in this article. All views and forecasts reflect the state of knowledge at the time of publication and are subject to change. There is no guarantee that future developments will unfold as described. Investing in commodities involves risks. Consultation with a licensed financial advisor is strongly recommended.