Disseminated on behalf of Commerce Resources Corp. and Zimtu Capital Corp.

A few years back, during the market run of 2011, the bellwether in the rare earth element (REE) space was arguably Molycorp Inc. with its Mountain Pass Mine in California, USA. Having been a producing mine (1950/60s to 2002), that continued to produce from stockpiles even after closure, Mountain Pass was the western project (i.e. non-Chinese) best positioned to capitalize on the rapidly ascending REE prices. Unfortunately on June 25, 2015, Molycorp announced it was filing for Chapter 11 bankruptcy, bringing an end to the Mountain Pass Mine and the once heralded saviour of REE to the non-Chinese world.

The immediate question that comes to mind is: How could this happen? And, if Molycorp could not succeed, how in the world can any other REE junior, with a non-Chinese REE deposit, hope to succeed?

This article seeks to answer these two fundamental questions, with a straight up comparison between Molycorp’s Mountain Pass Mine and Commerce Resources’ Ashram Deposit, but it will also pose another set of questions that all relate to “Why does the world continue to allow itself to be dominated by China”?

Prelim Bout – China the Schoolyard Bully

Let us begin in reverse order and look at the history of the REE bubble and consider first the questions “Why does the world continue to tolerate a commodity bully?” and ”When is the next crisis going to occur, that will again drive REE prices skyward?”

It has been said that “power corrupts and absolute power corrupts absolutely” and I believe that with the market events that started this week with China basically pulling the rug out from the rest of world’s markets – and their own people – everyone’s mind should be occupied with the issues of how this happened, and what is everyone going to do so that this does not happen again.

We know who the losers were when Molycorp went from $76 a share to Chapter 11, but who were the winners? The clear winners throughout the whole REE bubble are certainly the ones who continue to dominate the market and who manufactured the reasons that caused the bubble – the Chinese.

As China is the country that dominates the global REE market, they have benefited the greatest when REE prices soared over 1,000% and in some cases 3,000%, and they still benefit today. The ‘reality’ of prices falling for the last 4 years is that prices are still up 100%, 200%, and as much as 300% over the last 6 years for many of the REEs but especially for the magnet feed materials (MFREE; i.e. neodymium, praseodymium, terbium, and dysprosium). What other commodity has seen this kind of appreciation in this time frame?

The “Fishing Boat” incident in September 2010:

“The 2010 Senkaku Boat Collision Incident (or the Minjinyu 5179 Incident) occurred on the morning of September 7, 2010 when a Chinese trawler, Minjinyu 5179, operating in disputed waters collided with Japanese Coast Guard’s patrol boats near the Senkaku Islands.”

What were the concerns of the Chinese, over and above gaining the release of the crew and Captain of this potentially illegal fishing vessel operating in disputed Japanese territory? Was China concerned about their national security? Were they concerned about an expansionist west through the proxy of Japan? No, I believe that China saw an opportunity to address a long held interest to gain more value from the one commodity that they are dominant in – the REEs – and to increase their value-add for this commodity, which would ultimately bring more manufacturing to China and creat more jobs for Chinese citizens. And all they had to do was cut off Japan for supplies of REEs for a short period of time.

It would be hard to imagine a more successful effort at instilling anxiety and fear in the rest of the world than this incident, which was so simple and so inexpensive, and so very, very effective.

This shot across the bow was one that was heard by the whole world, imprinting in everyone’s DNA the need for alternate sources of REEs. And the take away from this event is still very valid: Why allow one country to dominate any commodity? Do Albertans wake up every day and say a prayer in the direction of OPEC?

And besides the market machinations of this week, what about the increasing tensions along the Korean peninsula? Does anyone believe that Kim Jong-un does anything of significance without the tacit approval of Beijing? Is this the new “crisis”?

The western world needs new sources of REEs. Unfortunately, this is not Molycorp. Fortunately, we still have Ashram.

Round One: Molycorp versus Commerce Resources: Mountain Pass versus the Ashram Deposit

Before the Mountain Pass Mine was brought back into production exactly 3 years ago (on August 27, 2012) for around half a billion dollars, Molycorp successfully sold a business plan to the United States, and the rest of the western world, that was promoted as being the answer, the solution, or you may call it the White Knight of a full-spectrum REE supply to the world. The sad fact is that Molycorp was not able to be this saviour. “In race of life, it does not matter who finishes first. What matters most is being able to complete your race.” (Lailah Gifty Akita)

However, before we continue with this direct comparison of the attributes of Mountain Pass against the Ashram, let us side bar for a brief interlude on “The Road to Hell”.

“The Phoenix Project”: Another Headstone in the “New” Failed Technology Graveyard

Molycorp was essentially its own worst enemy in that its continued production of cerium and lanthanum (at a loss) only added more cerium and lanthanum to an already over-supplied market, thereby helping to drive down their prices.

These are as close to the facts concerning Molycorp as you are likely to get for the current time being, but this is not the ‘real’ story of the fiasco by the name of Molycorp. The ‘real’ story of this demise should be placed under the heading – under which we have seen many chapters written many times before – of the “Failed New Technology”.

In the specific case of Molycorp, this is the “Phoenix Project”, and as the mythical creature the Phoenix rises from the ashes, so too was this supposed to be the saviour of non-Chinese REE production. However, this was not to be.

In 2010, in the heady run-up to the peaks of prices for the REE’s, Molycorp re-entered the public eye with the promise of operating costs that were speculated to be “half” of the average Chinese cost, or specifically “2.77 per kilo” and with “Superior Technology and Commercial Advantage” – these are literally quotes from a 2010 Molycorp presentation, which was about as widely disseminated as Gideon’s Bible in the day. Molycorp’s actual operating cost at Mountain Pass was rather in the +$30 range to produce a kilo.

In this case, which turns out to be perhaps the best example of “the road to hell is paved with good intentions”, Molycorp simply failed to commercialize this Phoenix (rising from the ashes and never quite taking flight before returning back to the ashes) is Molycorp’s overall problem and the reason for its demise. In this instance there is no specific antagonist, no specific “whistle-blower”, who knew or figured out the truth before you and I, and the rest of the investing public, realized that the emperor had no clothes. There is no Ravi Sood for example, who basically single-handedly shorted the failed silicon processor Timminco down from $36 a share to pennies. There is just a failed technology and millions of dollars evaporated. And how many times have you heard this story before?

There is simply no joy in Mudville on this one. There are just too many losers.

Round Two: Molycorp versus Commerce Resources: Reality Trumps Fallacies

Let us start this discussion by dispelling two fallacies in the space that foster the notion that all REE deposits are the same, and that “grade is king”. These are both highly inaccurate ideas as REE deposits are typically very different, with one in particular (i.e. the Ashram Deposit of Commerce Resources Corp.) perfectly placed to capitalize on Molycorp’s failure I would argue.

As alluded to prior, Molycorp’s woes may be best summed up to a series of unfortunate realities: Poor REE distribution, excessive debt, problematic jurisdiction, market timing, cost of production, and operational delays to name a few. Essentially, Molycorp found itself in an unsustainable bubble that burst rather than undergo a controlled deflate due its inability to navigate the situation it built, a situation that went far beyond the REE pricing environment, yet which was firmly rooted in the fundamentals of the deposit.

At the end of the day, Mountain Pass did not produce enough of the individual rare earths that the market wanted, compared to the rare earths that they were producing, which (unfortunately) were the REEs that the market did not want. In other words, the REE distribution of Mountain Pass was extremely unfavourable for the market, resulting in the forced processing of excessive amounts of the low-value REEs (Ce and La) in order to produce reasonable quantities the more valuable REEs (Nd, Pr, Tb, Dy). In turn, this resulted in a cost of production (per kg Nd-Pr-Tb-Dy produced) that was not sustainable when coupled with their numerous other burdens. However, this only increases the urgency to consider the following: What makes Commerce’s Ashram REE Deposit better positioned for success?

The overarching answer is that Commerce and Ashram have a much stronger ability to produce the REEs the market wants at potentially the lowest-cost in the entire space, certainly much lower than Mountain Pass. This is because Commerce and its Ashram Deposit are markedly different entities compared to any other REE company/project combinations globally.

The key to success, for any REE project, has always been low-cost production of the REEs that are in the shortest supply, highest demand, and with the most stable markets and growth profiles. Prior articles have discussed what sets Ashram apart from its peers, and time has only strengthened my opinion that Ashram is the top candidate for production. This article will endeavour to directly compare Ashram to Molycorp, a former REE powerhouse, and further explain why I believe Commerce and Ashram will succeed where Molycorp and Mountain Pass have failed.

Specifically, several distinct and key attributes that sets the Ashram Deposit apart, aka the “Ashram Advantage”, are as follows:

• A superior REE and pricing distribution, focused on the REEs with strongest and most stable markets (i.e. the magnet feed REEs; Nd, Pr, Tb, Dy)

• A higher absolute grade of the key heavy rare earth elements (HREEs); terbium (Tb) and dysprosium (Dy)

•A more conservative and, arguably, practical “mine to market” scenario

• Located in a more favourable jurisdiction (northern Quebec, Canada, as oppose to California, USA)

• A larger tonnage (>200 million tonnes vs. 30 million tonnes) with more contained total REO

• Positioned to better control and structure debt

Producing what the Market wants: REE Distribution and the Magnet Feed REEs

The first and foremost difference between Ashram and Mountain Pass is the REE distribution; defined as the proportion of each REE relative to all the REEs combined (15 elements in total, namely La through Lu plus Y collectively termed “TREE”).

REE distributions are commonly evaluated using the measures below (referenced to TREE):

• Light REE (LREE):

La, Ce, Pr, Nd, Sm, Eu, Gd

• Heavy REE (HREE):

Tb, Dy, Ho, Er, Tm, Yb, Lu, Y

• Middle + Heavy REE (MHREE):

Sm, Eu, Gd, Tb, Dy, Ho, Er, Tm, Yb, Lu, Y

• Critical REE (CREE):

Nd, Eu, Tb, Dy, Y

• Magnet Feed REE (MFREE):

Nd, Pr, Tb, Dy

Simply put, a deposit with an REE distribution more weighted in the REEs with the strongest and most stable markets that are in the highest demand yet shortest supply, will be in a significantly better positioned to produce the REEs the market wants at the lowest cost, all else being equal.

Over the last 8 plus years, more value has been given to deposits with the higher proportions of HREE or MHREE compared to TREE. This was largely because of the higher $ value per kg for those elements compared to all others. This measure of potential value has more recently been coupled with MFREE, and to a lessor extend CREE, which includes those REEs that are forecasted to have the strongest demand, as well as most stable markets and prices, over the near, middle, and long-term. The MFREE market, used in high-strength magnets, is forecasted to grow up to 8-12% annually.

Therefore, the market trends and pricing environment favour an REE distribution that is well balanced in these key REE elements. This is what the market wants, and therefore a properly balanced distribution, as in Ashram, should be a prominent key to success. Too much enrichment in the light REEs or the heavy REEs severely limit a project’s ability to adjust to a dynamic market and pricing environment over the course of a mine’s life. However, a well-balanced distribution focused on the key REEs, spread across the entire light and heavy REE spectrum is far more likely to be the REE distribution “sweet” spot required for success.

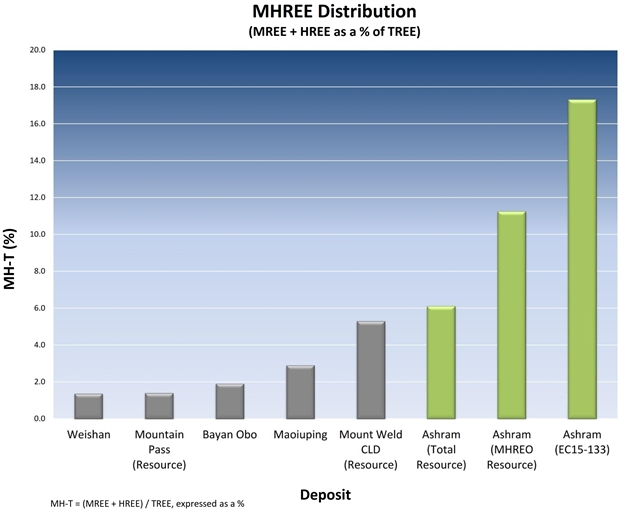

The below Figures 1, 2, and 3 illustrate clearly that, compared to Mountain Pass, Ashram has ~400-1,300% more enrichment in the group of REEs that have the highest $ value per kg (MHREE), as well as ~34-53% more enrichment in the REEs that have the strongest, largest, and most stable near-term, medium-term, and long-term markets (MFREE).

The impact of hosting a more well-balanced REE distribution is that more value may be extracted from the ore at a lower cost, relatively speaking. This means that fewer dollars are needed to process the unwanted REEs that come along for the ride. The more Ce there is compared to other REEs, the more Ce has to be processed alongside the more valuable MFREEs (Nd, Pr, Tb, Dy).

A poorly balanced distribution, as in Mountain Pass, means more of the low-value, less-stable market REEs (i.e. Ce, La) need to be produced in order to produce the high-value, stable market REEs (Nd, Pr, Tb, Dy). By comparison, Ashram is significantly more enriched in Nd, Pr, Tb, and Dy, and significantly less enriched in Ce and La. This is a key fundamental difference that will directly impact cost of production as well as operating margins as it is the dominate economic driver of an REE deposit.

Bottom-line: Ashram hosts a superior REE distribution compared to Mountain Pass using all industry standard measures (HREE, MHREE, CREE, and MFREE).

Further, the following Figure 4 illustrates that Ashram hosts a superior REE distribution compared to all other producing hard-rock mines globally (Lynas, Wieshan, Maoniuping, Bayan Obo). In other words, if Ashram was in production today, it would host the strongest REE distribution of any major hard-rock producing REE mine globally, and moreover, be most closely aligned with the REEs the market wants currently, or is forecasted to for the near, medium, and long-term (i.e. MFREE).

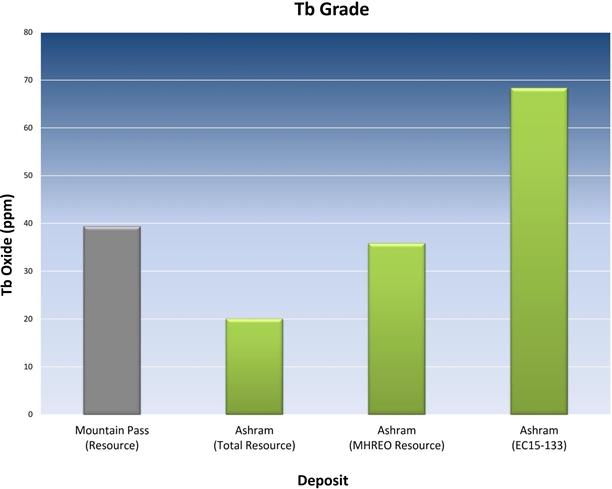

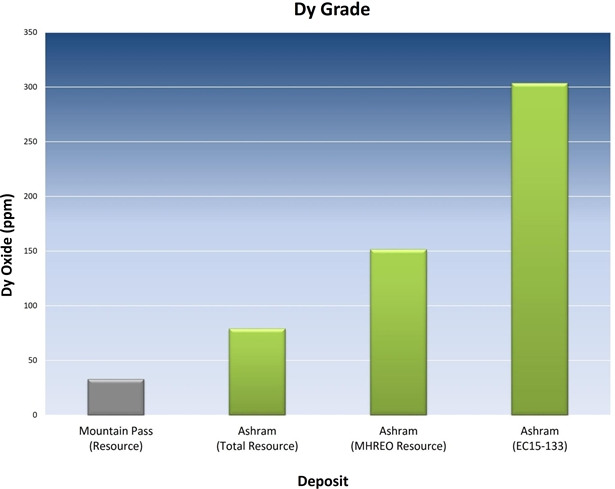

Absolute Total REE Grade

In absolute terms, Mountain Pass has greater amounts of Nd and Pr compared to Ashram, but has significantly less Tb-Dy by comparison (Figures 5, 6, 7, and 8). This is a result of the Ashram REE distribution being far more enriched in Tb and Dy (both MFREEs) by comparison. This attribute allows for Ashram the ability to process much less of the lower value REEs (Ce-La) to produce a kg of the higher value REEs (Nd, Pr, Tb, Dy).

In other words, compared to Mountain Pass, if Ashram were to enter production, it would produce a significantly higher proportion of the REEs that the market has the strongest demand and growth outlook for. Correspondingly, Ashram would produce less of REEs with the poorer market outlook in order to produce these higher value elements. This attribute is a major cost advantage for Ashram.

REE Pricing

Coupled with REE distribution and market strength is the pricing environment. Having the REEs the market wants would indicate a more stable pricing environment is present, and maximizing pricing stability is critical for any mining operation.

A review of the MFREE pricing trends over the last 5 years, with the pricing bubble of 2011 not included, reveals a much more stable pricing environment over the long-term than most realize; the REE prices for the MFREE are all higher than they were 5 years ago (Figures 9, 10, 11, and 12). How many commodities can this be said about?

Therefore, even though prices have declined considerably since the unsustainable highs of 2011, Nd-Pr-Tb-Dy all have positive price trends over the long-term that are forecasted to continue due to the strong demand and growth of magnets needed for the high-tech and clean-tech revolution.

Mine to Market Scenario

I discuss the various “mine to market” business plans in a prior article entitled “The Rare Earth Mine-To-Market Strategy and the Underlying Motives”.

Molycorp is more than just the Mountain Pass Mine in California. It owns an array of entities that target a full vertical integration model of mine to refined products for end use in an attempt to maximize value throughout the REE value chain, as well as dabbling in other rare metals. Such expanse will inevitably dilute focus on key operating requirements. In this case, it was the very front end of the process; that being the Mountain Pass Mine.

In essence, Molycorp targeted a full vertical integration before they had a handle on the front end. The company took on too much debt, over-promised, and under-delivered; never nearing the production targets they so loftily set.

As with any company, it is best to excel in the core business before expanding to other related endeavours. Commerce is not targeting full vertical integration but rather a mixed rare earth concentrate as its final product, potentially toll processing or selling outright to companies with excess separation capacity.

If any company hopes to succeed further down the value chain, they must first master an economic business model at the mixed concentrate stage. If more value chain is required to be profitable, the business is unlikely to succeed.

Jurisdiction

Apart from all the technical merits, the often overlooked aspect of jurisdiction should not be neglected. The 2014 Annual Survey of Mining Companies, carried out by the Fraser Institute, notes Quebec in 6th spot (Ashram) out of 122 jurisdictions that were part of the survey, with California in 48th spot (Mountain Pass). This survey is widely regarded by industry as a good measure of a mining friendliness and favourableness.

Let’s not forget that the state of California had a large hand in contributing to the closure of the Mountain Pass Mine in 2002. This time around, the regulatory environment and the ongoing severe draught in California could not have helped Mountain Pass, given the significant amount of water required for operations.

Alternatively, REEs are verbally and financially supported by the Government of Quebec, through public disclosure and formal financial investments into the projects. The presence of Ashram is growing and one can bet that the Government of Quebec has taken notice.

Debt

Molycorp’s chances of success were severely retarded due to the mountain of debt; to the tune of $1.7 billion, that the company piled on for the modernization of its mine and processing facilities, as well as numerous acquisitions related to its full vertical integration mine to market scenario. This resulted in a poor balance sheet with limited ability to handle operational overruns, production delays, and periods of depressed pricing that are common to every industry.

Commerce Resources Corp. is starting clean with no debt and the ability to appreciate what can happen when fiscal responsibility is not maintained. The company is targeting a mixed rare earth concentrate product in the early production years in order to limit capital requirements at start-up and, for lack of a better phrase, not bite off more than they can chew.

Tonnage

According to Technology Metals Research (TMR), Mountain Pass’ resources stand at approximately 32 million tonnes (Mt) at 6.6% TREO for a total of 2.1 Mt contained REO, while Ashram’s resources stand at approximately 240 Mt at 1.9% TREO for a total of 4.5 Mt contained REO.

The Mountain Pass pit is already ~450m across and ~120m deep meaning further excavation is required to mine the 32 Mt of resources remaining. All of the Ashram Deposit material is sitting right at surface, and there is simply far more of it (i.e. lower cost mining for longer).

Conclusion

Anyone familiar with the REE space will know that grade is rarely “king” as they say. A deposit’s REE distribution is essential as one REE cannot be separated easily from another. I believe the fundamental reason Molycorp failed with its Mountain Pass Mine revival is because it had to produce too many of the REEs (Ce, La) the market did not care for, while trying to produce sufficient quantities of the REEs (Nd, Pr, Tb, Dy) the market wanted, in order to attain profitability. This resulted in higher operating costs, and lower overall operating margins that were simply not sustainable in this market environment.

Commerce’s Ashram Deposit is markedly different from Molycorp’s Mountain Pass Deposit and this is highlighted by a superior REE distribution more focused on what the market needs now, and will need more in the future. Coupled with the knowledge of why Mountain Pass failed, apart from REE distribution, this may effectively strengthen the potential for Ashram to enter production and avoid the fatal missteps of Molycorp.

At the end of the day, the end-users complacency to enter to the market is temporary, as there is simply not enough supply, or supply stability, to offset demand in the mid to long-term. Therefore, now is the time to identify the projects most poised to capitalize on the REE market turnaround that is coming, and in my opinion, the Ashram Advantage is crystal clear.

Direct link to above chart (15 min. delayed): http://schrts.co/wR62L5

Research #10 “Interview with Darren L. Smith and Chris Grove while the Graveyard of REE Projects Gets Crowded“

Research #9 “The REE Basket Price Deception & the Clarity of OPEX“

Research #8 “A Fundamental Economic Factor in the Rare Earth Space: ACID“

Research #7 “The Rare Earth Mine-to-Market Strategy & the Underlying Motives“

Research #6 “What Does the REE Market Urgently Need? (Besides Economic Sense)“

Research #5 “Putting in Last Pieces Brings Fortunate Surprises“

Research #4 “Ashram - The Next Battle in the REE Space between China & ROW?“

Research #3 “Rare Earth Deposits: A Simple Means of Comparative Evaluation“

Research #2 “Knocking Out Misleading Statements in the Rare Earth Space“

Research #1 “The Knock-Out Criteria for Rare Earth Element Deposits: Cutting the Wheat from the Chaff“

Disclaimer: Please read the full disclaimer in the full research report as a PDF (here) or on www.rockstone-research.com or within the full research report on Zimtu Capital Corp. (June 17, 2015), as multiple conflicts of interest exist. The author, Stephan Bogner, owns shares of Commerce Resources Corp., as well as Zimtu Capital Corp., and would benefit from a share price increase of either company. The author is paid by Zimtu Capital Corp., which publicly traded company also owns shares of Commerce Resources Corp., and would also benefit from price appreciation and volume, whereas Zimtu Capital Corp. and the author could sell shares anytime without notice. Therefore, the above information is not to be construed as independent financial analysis but strictly as an advertisement.