Neodymium-Iron-Boron Magnets (source)

Last week, at the Langham Hotel in Hong Kong, the most important rare earth element (REE) conference of the year took place; the 12th International Rare Earths Conference hosted by Metal Events Ltd. It was an excellent opportunity to get a complete overview and update on all the market metrics regarding this essential group of commodities, including information on the few remaining active projects in the sector.

First, it was clearly outlined that actual REE demand and usage has increased at a robust CAGR (compound annual growth rate) over the past 6 years. This is in stark contrast to the most obvious aspect for the REEs over the same time period, that being their falling prices. As it was opined, prices for several key REEs appear poised for a strong rebound to more sustainable levels over the medium to long-term.

Secondly, the overwhelming consensus is that demand will continue to increase at a robust CAGR, especially with respect to the magnet feed rare earths, principally neodymium (Nd) and praseodymium (Pr) but also dysprosium (Dy) and terbium (Tb).

Thirdly, although considerable research has been completed over the past 6 years to identify economically viable substitutes for magnet feed REEs, none have been found, excepting for the partial substitution using cerium (Ce), which is also an REE. Moreover, cerium as a substitute produces inferior results, thus, limiting its usage. Further, besides the fact that it is widely accepted that there are no viable substitutes for the REEs in permanent magnets, with prices back down to current levels, there is no incentive to look for substitutes anymore.

Additionally, given the forecasted supply of Ce and lanthanum (La) to the market, driven by the production of Nd and Pr for permanent magnets, there has been significant research and development focused on new applications for those specific REEs. These include Ce-Al alloys for the aerospace industry as well as polyvinyl chloride (PVC) stabilizers using Ce and La to protect and prevent degradation of the PVC.

The last several years have seen a massive paradigm shift in the REE market, which only a few predicted and were positioned for – that being, the declining use of REEs in the phosphor market (Eu, Tb, Y) and the persistent push to engineer out, or limit, the use of Dy and Tb in rare earth permanent magnets.

This in effect has relegated those projects whose economics are primarily driven by the heavy REEs of Dy and Tb to the back seat, as it is the light REEs, specifically Nd and Pr, that continue to have, and are forecasted over the long-term to have, the fastest growing market. This is also a market that is continually developing new applications for the permanent magnets that these REEs are essential for.

And thus, perhaps of greatest significance to the rare earth industry over the near, mid, and long-term, is the developing and expanding applications built on the foundation of rare earth permanent magnets. Two of the most prominent include magnetocaloric chillers (refrigerator units), and industrial robots. Such emerging applications, specifically refrigeration, have only recently begun to forge their market penetration (currently <1%), where others such as industrial robots are poised for explosive growth.

For 2016, the International Federation of Robotics notes a Robot Density (# of multipurpose industrial robots per 10,000 persons employed in manufacturing industry) for China of 49, whereas Singapore and South Korea are 398 and 531 respectively, thus, highlighting the room for considerable growth. Adamas Intelligence is forecasting the annual industrial robot shipments to China to increase from 68,500 units in 2015 to 505,000 units by 2025, for a staggering CAGR of 22.1%. This equates to an additional annual rare earth permanent magnet demand of more than 8,000 tonnes by 2025. When coupled with magnetocaloric chillers, Adamas forecasts that rare earth permanent magnet demand will grow by more than 14,000 tonnes by 2025 from only those 2 applications alone.

Alternatively, in terms of a reasonable expectation that may have a greater psychological meaning than fundamental economic importance, it is argued that Tesla Motors will move to replace their AC induction motor, which does not use REEs, to a permanent magnet motor that requires rare earth permanent magnets. Although cheaper, the AC induction motor is larger, heavier, and less efficient resulting in more draw on the lithium ion battery pack, when compared to a permanent rare earth magnet motor. Apart from Nikola Tesla having invented the first AC induction motor, Tesla Motors likely chose the induction motor over the permanent magnet motor due to the existing REE prices when their first electric vehicle was developed (Model S). As REE prices have fallen, the market fundamentals are now positioned for a long-term sustainable REE pricing environment where the benefits of rare earth permanent magnet motors far exceed the elevated cost compared to the AC induction motor currently relied upon.

Overall, REEs form the foundation of the high-tech industry and the accompanying global “green revolution” to reduce greenhouse gas emissions along with lithium, and it is expected that we will now see price appreciation for the REEs.

Depending on the market analyst, current global demand is estimated at 130,000-150,000 tonnes REO per year, with magnet feed REOs, primarily neodymium (Nd) and praseodymium (Pr) and to a lesser extent terbium (Tb) and dysprosium (Dy), comprising the dominant growth market at 6-12% CAGR.

The dominant economic driver for the Ashram Rare Earth Deposit of Commerce Resources Corp. is the magnet feed REOs due to a unique and well-balanced REO distribution focused on those key REOs. When compared to major global producers, the Ashram Deposit’s MHREO Zone resource has the highest magnet feed REO distribution at 24.7% NdPrTBDy combined.

The heavy REO focused rare earth deposits promoted so heavily during the bubble are yesterday‘s news. Today, and for the foreseeable future looking decades ahead, it is the deposits anchored with the magnet feed REOs that are best positioned for stock price breakout, and ultimately production.

A Rare Earth Market Inflection Point?

• Leading analysts are forecasting a 3-7% CAGR for REO demand out to 2025 (195,000-280,000 tonnes REO per annum). This will be highlighted by the explosive growth of rare earth permanent magnets (Nd, Pr, Tb, Dy) in applications such as refrigeration and industrial robots, as well as PVC stabilizers (La, Ce) and specialty alloys (Ce-Al) for other LREE.

• Many individual REO prices remains significantly higher than they were pre-bubble (pre-2009) and now appear to have bottomed from their 5-year decline, giving further credence to an upward breakout.

• Numerous market analysts forecast a neodymium oxide price of $60-90 USD/kg for sustainability over the long-term, which is considerably higher than where it is today ($35-40).

• China continues to progress with its rare earth industry consolidation and its clampdown on illegal production that has depressed the overall REO pricing environment. As supply is removed from the market, prices will gain upward momentum.

• It is widely believed that Chinese rare earth companies are losing money, and losing money is certainly not part of a sustainable business model.

To put this more into perspective, one only needs to look at the price/demand paradox of the rare earth market today, where REO demand has continued to increase while REO prices have fallen. This is clearly unsustainable, and as the consensus is overwhelmingly in favour of long-term robust demand growth, the prices of REO (moreover the magnet feed REO) are poised for a sustainable breakout to the upside for the long-term.

I continue to emphasize Commerce Resources Corp.’s Ashram Rare Earth Project as my top pick in the rare earth space. Their unique and well-balanced REO distribution affords them greater market flexibility, and is anchored by those rare earths that have the strongest market fundamentals over the near, mid, and long-term.The project is located in a great jurisdiction, is large, of good grade, and hosts a simple rare earth mineralogy that has been demonstrated upgradeable into high-grade mineral concentrate (>45% REO) comparable to producers that is of high recovery (>75%). No other rare earth project in development can process their material as effectively as that done with Ashram, and this has led to the Ashram Project having the lowest projected OPEX in the space based on their PEA.

I believe the inflection point is nearly upon us, and thus, the opportunity is now and with Commerce Resources Corp.

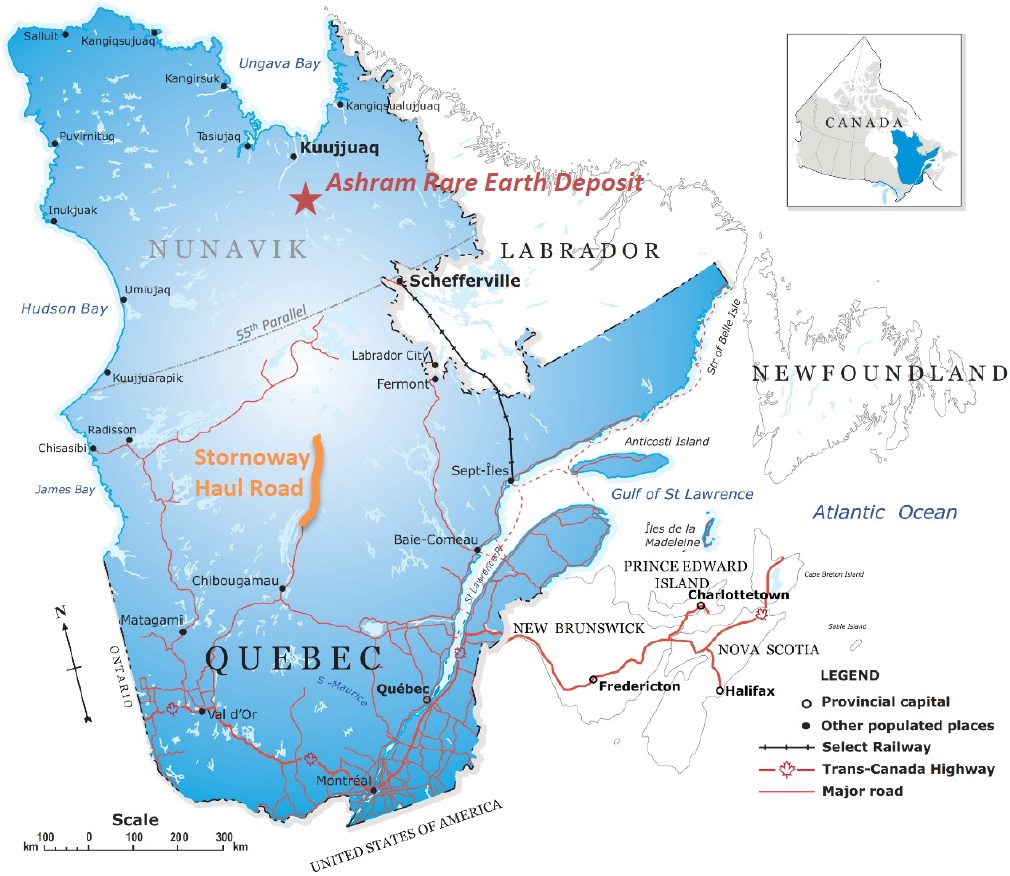

The Ashram REE Deposit is approximately 130 km south of Kuujjuaq, the administrative centre of Nunavik. The Québec government, through the Société du Plan Nord, arranged financing and construction of the 245 km long road for the Renard Diamond Project owned by Stornoway Diamond Corp. Québec government’s Société du Plan Nord mandated to invest in the northern infrastructure development, first and foremost for the energy and mineral resource development and for transportation infrastructure and access.

Will permanent magnets save the rare earth industry?

By Paul Dvorak on November 7, 2016, for WindPowerEngineering.com

These ferrite magnets come from BLS Magnet.

Rare earths: Market Outlook to 2026, 16th Edition, 2016 is available from Roskill Information Services Ltd, 54 Russell Road, London SW19 1QL UK. Click here to download the brochure and sample pages.

The permanent magnet and catalyst sectors will continue to provide the largest markets for rare earths in the next ten years to 2026. Catalysts will continue to drive growth in the light rare earth elements lanthanum and cerium, while permanent magnets will lead growth in neodymium, praseodymium and dysprosium.

Supply of some rare earths is far greater than that of others as a result of production methods and there is a discontinuity between supply and demand across the different elements. Despite growth in catalyst (and, to a lesser extent, polishing and nickel metal hydride battery) demand, cerium and lanthanum will remain in substantial surplus to 2026. Demand for neodymium, however, is beginning to outstrip supply.

Rapid growth expected from permanent magnets, but will it be short-lived?

In the short-term to 2021, neodymium-iron-boron (NdFeB) magnet demand is forecast to grow strongly. The traditional consumer electronics and automotive sectors account for the majority of NdFeB demand, but these magnets will experience strong growth from the emerging green technologies of wind turbines and new energy vehicles (NEVs).

Between 2016 and 2021, global NdFeB magnet production is forecast to grow by 4 to5% per year. Global NEV production could rise by 3.5 to 4.0 million vehicles, while global wind power installations could increase by 0.4 million MW according to Roskill’s new rare earth report. Chinese NEV consumption will see high growth rates as these vehicles are exempt from city number plate lotteries. The Chinese government is also offering a range of tax cuts and purchasing incentives to encourage the uptake of NEVs.

As a result of increasing consumption, neodymium is expected to fall into deficit in 2016, although demand will initially be met by the drawdown of stocks. The deficit is forecast to increase to 2021, making continued growth of NdFeB magnets unsustainable, despite efforts by rare earth producers to increase neodymium supply.

The neodymium price will rise towards the point of inflection, above which, magnet consumers will begin to replace NdFeB magnet technologies with substitutes. The green energy sector is the most vulnerable to price rises because of the large size of magnets used. Technologies already in use in this industry as an alternative to permanent magnet motors include induction motors in NEVs and induction/synchronous generators in wind turbines.

By 2021, it is expected that the high price of neodymium and concerns over supply availability will make projected growth rates of NdFeB demand unsustainable and demand for NdFeB magnets will fall rapidly from 2022, before stabilising at a much lower growth rate. Overall, NdFeB magnet growth between 2021 and 2026 is forecast to be flat, possibly falling by up to -1% per year.

Demand for dysprosium will also grow from the use of magnets in high temperature applications (including NEVs) but manufacturers are actively trying to reduce dysprosium-containing magnet consumption wherever possible and to develop new ways to reduce intensity of dysprosium use. Little to zero dysprosium is consumed in wind turbines; maximising airflow allows for a lower operating temperature in this application.

Neodymium prices rising but other rare earth prices will see little excitement

The price of neodymium (and, to a lesser extent praseodymium and dysprosium) will rise with increasing NdFeB magnet demand to 2026. The price for most other rare earth elements, however, will decline over this period. Lanthanum and cerium prices will be limited by surplus supply. Prices for europium and terbium will fall considerably as demand from the phosphors industry continues to decline rapidly. These two elements were previously perceived to be critical because of their high use and low availability. The recent shift in the lighting industry, from fluorescent to LED lamps, however, has reduced demand for rare earth phosphors by around two thirds since 2011.

China still dominates and this isn’t about to change

China dominates global rare earth supply, accounting for an estimated 88% in 2016. China’s position weakened slightly in the 2010s as ROW production increased with the start of mining by Lynas in Australia and by Molycorp in the U.S. Molycorp has since declared bankruptcy and closed its operations in 2015.

Low prices for most rare earths to 2026 will discourage investment in new projects and the rare earth industry in the ROW is not expected to see a significant injection of new capacity. Current producers may expand where possible to serve increasing neodymium demand.

Illegal mining remains one of the main threats to rare earth prices going forward. The Chinese government has committed to reduce illegally sourced material by introducing a raw material tracing system and granting great powers to raid and prosecute illegal miners, separators and distributors.

Mining from unofficial sources accounts for 25 to 30% of global rare earth supply in 2016 and is mainly carried out in the south of China where a large number of companies extract small quantities of heavy rare earths.

The Chinese system of export quotas and taxes was scrapped in 2015 after China lost an appeal with the WTO. Chinese exports of rare earth compounds, metals and alloys are expected to rise by 17,100 tons in 2016 but are unlikely to see a significant increase in future years as the vast majority of consumption takes place in China. The Chinese government continues to encourage downstream processing and the export of manufactured goods over raw materials. Some of the increase in 2016 may be a result of China filling the void left by Molycorp’s closure. For more: www.roskill.com

China plans to fast-charge electric vehicle production

By Bloomberg New Energy Finance on August 17, 2016 (source)

China is said to be considering the introduction of compulsory quotas for carmakers that would require them to produce more electric vehicles or purchase carbon credits from their peers, in a bid to tighten emissions and support companies in developing what the government considers a strategic industry.

The proposed measure will require certain automakers to produce or import new-energy vehicles in proportion to the number of fuel-burning cars they sell, according to a draft document prepared by China’s National Development and Reform Commission.

Companies that fail to achieve the carbon dioxide emissions reduction targets would be required to buy credits or pay fines of as much as five-times the average price of the credits, the country’s top industry regulator and policy maker said.

China’s government has been announcing policies to accelerate the sale of electric vehicles and last year, it surpassed the US as the largest market for electric vehicles. According to Bloomberg New Energy Finance, electric vehicle sales in China in Q1 2016 saw a year-on-year increase of 181%. Our latest outlook on the electrified transport market can be read here . The world’s most populous nation wants sales of new-energy vehicles to exceed 3m units a year by 2025. To encourage production and sales, its central and local governments have spent CNY 15bn ($2.3bn) on subsidies since 2009, according to state-run China Central Television. However, Chinese officials plan to scale back subsidies for electric vehicles by 2020, and this initiative will mark a transition away from a subsidy-driven approach to catalysing sales of cleaner cars.

Elsewhere in Asia, the Indian Renewable Energy Development Agency (IREDA) said it would issue as much as $150m in offshore rupee bonds by November to support the nation’s plans for green power, according to a top official. IREDA – a government agency that extends financial assistance for renewable energy and energy efficiency projects – approved loans worth INR 78bn in the financial year ending March 31 while also disbursing INR 43bn to borrowers. Its lending represents a year-on-year increase of 60%, according to Ireda Director of Finance Satish Kumar Bhargava. The bonds follow INR 17.16bn already raised by IREDA in January. The bonds will be issued on either the London Stock Exchange or the Singapore Stock Exchange, he said.

Meanwhile, in Europe, UK Prime Minister Theresa May has written to Chinese President Xi Jinping and Premier Li Keqiang to express her desire to enhance trade and strategic ties, Britain’s new Asia envoy said. Alok Sharma, on his first official visit to China since being appointed Minister for Asia and the Pacific last month, told Chinese Foreign Minister Wang Yi in Beijing that the UK attaches great importance to cooperation with Beijing, according to an online statement by China’s foreign ministry. Sharma called China an “important global strategic partner.” The message comes as May last month postponed approval of the GBP 18bn ($23bn) Hinkley Point nuclear power plant in southwest England – the first to be built in the country in three decades. The decision stunned Chinese and French backers, who had hoped to sign construction contracts immediately.

Also in the UK, Macquarie Group reached financial close on the GBP 900m ($1.2bn) biomass power plant, located in northern England. The Tees Renewable Energy Plant, which will run on wood pellets and chips, will have a capacity of 299MW once complete.

Macquarie would have a 50% ownership stake with the remaining 50% held by Pensionskassernes Administration. The facility is expected to generate electricity for the equivalent of 600,000 homes according to the project website.In other large deals this week, the EUR 1.6bn ($1.8bn) Merkur offshore wind project, located in the German North Sea also reached financial close, contributing to a strong week for European renewable energy projects.

Switzerland-based Partners Group Holding invested EUR 250m for 50% of the wind project, according to a statement. InfraRed Capital Partners Ltd.’s Infrastructure Fund III took a 25% stake for EUR 125m. Belgium’s Dredging Environmental & Marine Engineering, General Electric. and the French Environment and Energy Management Agency also took stakes. The 400MW wind project is expected to power 500,000 homes once complete.

Total commitment to European renewable energy projects reached a record $7bn in 2015 — up 8% from 2014. Last year saw a lower level of direct equity investment in projects by institutions than the previous year but a higher value of commitments via ‘platforms’ — funds created by a lender or equity investor, in which the latter commits money alongside institutions like pension funds. 2015 also saw significant activity in project bonds. Already in 2016, more money has been committed in direct investment by institutions than the whole of last year — as quoted project funds have struggled to raise new equity in the same way they did before the summer 2015 crash of the yieldco.

Company Details

Commerce Resources Corp.

#1450 - 789 West Pender Street

Vancouver, BC, Canada V6C 1H2

Phone: +1 604 484 2700

Email: cgrove@commerceresources.com

www.commerceresources.com

Shares Issued & Outstanding: 259,508,950

Canadian Symbol (TSX.V): CCE

Current Price: $0.055 CAD (11/16/2016)

Market Capitalization: $14 million CAD

German Symbol / WKN (Frankfurt): D7H / A0J2Q3

Current Price: €0.039 EUR (11/16/2016)

Market Capitalization: €10 million EUR

Previous Coverage

Report #20 “Commerce records highest niobium mineralized sample to date at Miranna“

Report #19 “Carbonatites: The Cornerstones of the Rare Earth Space“

Report #18 “REE Boom 2.0 in the making?“

Report #17 “Quebec Government starts working with Commerce“

Report #16 “Glencore to trade with Commerce Resources“

Report #15 “First Come First Serve“

Report #14 “Q&A Session About My Most Recent Article Shedding Light onto the REE Playing Field“

Report #13 “Shedding Light onto the Rare Earth Playing Field“

Report #12 “Key Milestone Achieved from Ashram’s Pilot Plant Operations“

Report #11 “Rumble in the REE Jungle: Molycorp vs. Commerce Resources – The Mountain Pass Bubble and the Ashram Advantage“

Report #10 “Interview with Darren L. Smith and Chris Grove while the Graveyard of REE Projects Gets Crowded“

Report #9 “The REE Basket Price Deception & the Clarity of OPEX“

Report #8 “A Fundamental Economic Factor in the Rare Earth Space: ACID“

Report #7 “The Rare Earth Mine-to-Market Strategy & the Underlying Motives“

Report #6 “What Does the REE Market Urgently Need? (Besides Economic Sense)“

Report #5 “Putting in Last Pieces Brings Fortunate Surprises“

Report #4 “Ashram – The Next Battle in the REE Space between China & ROW?“

Report #3 “Rare Earth Deposits: A Simple Means of Comparative Evaluation“

Report #2 “Knocking Out Misleading Statements in the Rare Earth Space“

Report #1 “The Knock-Out Criteria for Rare Earth Element Deposits: Cutting the Wheat from the Chaff“

Stay Tuned!

For smartphones and tablets, an APP from Rockstone Research is available in the AppStore and in the GooglePlayStore.

Disclaimer: Please read the full disclaimer within the full research report as a PDF (here) as fundamental risks and conflicts of interest exist.